EXHIBIT 99.2

Published on September 8, 2020

Exhibit 99.2

Monocle Acquisition Corporation AerSale Corp. Investor Presentation September 2020

2 No Offer or Solicitation This investor presentation (“Investor Presentation”) is for informational purposes only and does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any equity, debt or other financial instruments of Monocle Acquisition Corporation (“Monocle”) or AerSale Corp . (the “Company” or “AerSale”) or any of Monocle’s or AerSale’s affiliates . The Investor Presentation has been prepared to assist parties in making their own evaluation with respect to the proposed business combination (the “Business Combination”), as contemplated in the Amended and Restated Agreement and Plan of Merger (the “Amended and Restated Merger Agreement”), of Monocle and AerSale and for no other purpose . It is not intended to form the basis of any investment decision or any other decision in respect of the Business Combination . The information contained herein does not purport to be all - inclusive . The data contained herein is derived from various internal and external sources . No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any projections or modeling or any other information contained herein . Any data on past performance or modeling contained herein is not an indication as to future performance . Monocle and AerSale assume no obligation to update the information in this Investor Presentation . Information contained in this Investor Presentation regarding Monocle has been provided by Monocle and information contained in this Investor Presentation regarding AerSale has been provided by AerSale . Use of Projections This Investor Presentation contains financial forecasts with respect to AerSale’s projected revenues, Adjusted EBITDA, the EBITDA bridge and free cash flow for AerSale’s fiscal years from 2020 to 2024 . Neither Monocle’s independent auditors, nor the independent registered public accounting firm of AerSale, audited, reviewed, compiled, or performed any procedures with respect to the projections for the purpose of their inclusion in this Investor Presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this Investor Presentation . These projections should not be relied upon as being necessarily indicative of future results . These projections are illustrative purposes only and should not be relied upon as being necessarily indicative of future results . In this Investor Presentation, certain of the above - mentioned projected information has been included (in each case, with an indication that the information is a projection or forecast), for purposes of providing comparisons with historical data . The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information . Accordingly, there can be no assurance that the prospective results are indicative of the future performance of AerSale, Monocle, or the combined company after completion of the proposed Business Combination, or that actual results will not differ materially from those presented in the prospective financial information . Inclusion of the prospective financial information in this Investor Presentation should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved . Important Information About the Business Combination and Where to Find It In connection with the Business Combination, Monocle Holdings Inc . , the newly formed holding company that will become the parent of Monocle and AerSale at the closing of the Business Combination, filed with the SEC on December 31 , 2019 a Registration Statement on Form S - 4 , as amended by Amendment No . 1 to the Registration Statement on Form S - 4 , filed with the SEC on February 14 , 2020 which included a preliminary proxy statement/prospectus of Monocle . In connection with entering into the Amended and Restated Merger Agreement, Monocle Holdings Inc . will file Amendment No . 2 to the Registration Statement on Form S - 4 (as amended, the “Registration Statement”) . When available, the definitive proxy statement/prospectus and other relevant materials for the Business Combination will be mailed to stockholders of Monocle as of a record date to be established for voting on the Business Combination . You are advised to read, when available, the preliminary proxy statement/prospectus as it shall be revised, and the definitive proxy statement/prospectus and documents incorporated by reference therein filed in connection with the Business Combination, as these materials will contain important information about Monocle, AerSale and the Business Combination . Stockholders will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other documents filed with the U . S . Securities and Exchange Commission (“SEC”) that will be incorporated by reference therein, without charge, once available, at the SEC’s web site at www . sec . gov, or by directing a request to : Monocle Acquisition Corporation, 750 Lexington Avenue, Suite 1501 , New York, NY 10022 . Participants in the Solicitation Monocle and its directors and executive officers may be deemed participants in the solicitation of proxies from Monocle’s stockholders with respect to the Business Combination . A list of the names of those directors and executive officers and a description of their interests in Monocle is contained in Monocle’s preliminary proxy statement, filed with the SEC on December 31 , 2019 , as amended by Amendment No . 1 to the preliminary proxy statement, filed with the SEC on February 14 , 2020 , and is available free of charge at the SEC’s web site at www . sec . gov, or by directing a request to Monocle Acquisition Corporation, 750 Lexington Avenue, Suite 1501 , New York, NY 10022 . Additional information regarding the interests of such participants will be contained in the definitive proxy statement/prospectus for the Business Combination when available . AerSale and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the stockholders of AerSale in connection with the Business Combination . A list of the names of such directors and executive officers and information regarding their interests in the Business Combination will be included in the definitive proxy statement/prospectus for the Business Combination when available . Forward - Looking Statements This Investor Presentation includes “forward - looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 . Monocle’s and AerSale’s actual results may differ from their expectations, estimates and projections and consequently, you should not rely on these forward looking statements as predictions of future events . Words such as “expect,” “estimate,” “project,” “budget,” “forecast,” “anticipate,” “intend,” “plan,” “may,” “will,” “could,” “should,” “believes,” “predicts,” “potential,” “continue,” and similar expressions are intended to identify such forward - looking statements . These forward - looking statements include, without limitation, Monocle’s and AerSale’s expectations with respect to future performance and anticipated financial impacts of the Business Combination, the satisfaction of the closing conditions to the Business Combination and the timing of the completion of the Business Combination . These forward - looking statements involve significant risks and uncertainties that could cause the actual results to differ materially from the expected results . Most of these factors are outside Monocle’s and AerSale’s control and are difficult to predict . Factors that may cause such differences include, but are not limited to : ( 1 ) the impact of the COVID - 19 pandemic on the aviation industry and the aviation aftermarket industry generally, and on AerSale’s business in particular ; ( 2 ) the occurrence of any event, change or other circumstances that could give rise to the termination of the Amended and Restated Merger Agreement or could otherwise cause the Business Combination to fail to close ; ( 3 ) the outcome of any legal proceedings that may be instituted against Monocle and AerSale following the announcement of the Amended and Restated Merger Agreement and the Business Combination ; ( 4 ) the inability to complete the Business Combination, including due to failure to obtain approvals from the stockholders of Monocle and AerSale or other conditions to closing in the Amended and Restated Merger Agreement ; ( 5 ) the inability to obtain or maintain the listing of the shares of common stock of the post - acquisition company on The Nasdaq Stock Market following the Business Combination ; ( 6 ) the risk that the Business Combination disrupts current plans and operations as a result of the announcement and consummation of the Business Combination ; ( 7 ) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably and retain its key employees ; ( 8 ) costs related to the Business Combination ; ( 9 ) changes in applicable laws or regulations ; ( 10 ) the possibility that AerSale or the combined company may be adversely affected by other economic, business, and/or competitive factors ; and ( 11 ) other risks and uncertainties indicated from time to time in the proxy statement/prospectus relating to the Business Combination, including those under “Risk Factors” therein, and in Monocle’s other filings with the SEC . Monocle cautions that the foregoing list of factors is not exclusive . Monocle further cautions readers not to place undue reliance upon any forward - looking statements, which speak only as of the date made . Monocle does not undertake to release publicly any updates or revisions to any forward - looking statements to reflect any change in its expectations or any change in events, conditions or circumstances on which any such statement is based unless required to do so under applicable law . Important Notices and Disclaimers

3 Industry and Market Data In this Investor Presentation, we rely on and refer to information and statistics regarding market participants in the sectors in which AerSale competes and other industry data . We obtained this information and statistics from third - party sources, including reports by market research firms, and company filings . Non - GAAP Financial Measures This Investor Presentation includes non - GAAP financial measures, including Adjusted Revenue, Pro Forma Adjusted Revenue, Adjusted EBITDA and Pro Forma Adjusted EBITDA . AerSale defines Adjusted Revenue as revenue after giving effect to the AerLine Divested Revenue . AerSale defines Pro Forma Adjusted Revenue as Adjusted Revenue after giving effect to the Normalized Avborne Revenue and the Normalized Qwest Revenue . AerSale defines Adjusted EBITDA as net income (loss) after giving effect to interest expense, depreciation and amortization, income tax expense (benefit), management fees, the airline settlement and one - time adjustments and non - recurring items . AerSale defines Pro Forma Adjusted EBITDA as Adjusted EBITDA after giving effect to Normalized Avborne EBITDA, Normalized Qwest EBITDA and Public Company Costs . See Non - GAAP Financial Reconciliation on slide 37 . Monocle and AerSale believe that these non - GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to AerSale’s financial condition and results of operations . AerSale’s management uses certain of these non - GAAP measures to compare AerSale’s performance to that of prior periods for trend analyses and for budgeting and planning purposes . A reconciliation of non - GAAP forward looking information to their corresponding GAAP measures has not been provided due to the lack of predictability regarding the various reconciling items such as provision for income taxes and depreciation and amortization, which are expected to have a material impact on these measures and are out of AerSale and Monocle’s control or cannot be reasonably predicted without unreasonable efforts . You should review AerSale’s audited financial statements, which are included in the proxy statement/prospectus to be delivered to Monocle’s stockholders, and not rely on any single financial measure to evaluate AerSale’s business . Other companies may calculate Adjusted Revenue, Pro Forma Adjusted Revenue, Adjusted EBITDA and Pro Forma Adjusted EBITDA differently, and therefore AerSale’s Adjusted Revenue, Pro Forma Adjusted Revenue, Adjusted EBITDA, Pro Forma Adjusted EBITDA and other non - GAAP measures may not be directly comparable to similarly titled measures of other companies . Important Notices and Disclaimers (Cont’d)

4 Table of Contents I. Introduction & Situation Overview II. Business Overview & Growth Opportunities III. Financial Detail & Transaction Summary IV. Appendix

Section I Introduction & Situation Overview

6 Presenters and Senior Leadership Richard Townsend Chief Financial Officer ▪ 39 years of finance, operating and strategy experience ▪ Managing Partner at Rangeley Capital ▪ Former EVP & CFO of Loral Space & Communications (NASDAQ:LORL) ▪ Previously served as Corporate Controller & Director of Strategy at ITT Industries (NYSE:ITT) ▪ Formerly served as Controller of EMEA region at IBM (NYSE:IBM) ▪ 35 years of senior leadership and management experience ▪ Board Member at exactEarth Ltd. (TSX:XCT), Maxar Technology Inc. (NYSE:MAXR) and Sequa Corporation ▪ Previously held President & COO role at Loral Space & Communications (NASDAQ:LORL) ▪ Formerly was a Partner at Fried, Frank, Harris, Shriver & Jacobson Eric Zahler Chief Executive Officer and President Sai Devabhaktuni Chairman ▪ 25 years of investing experience ▪ Board Member at Sequa Corporation ▪ Previously was EVP & Head of Corporate Distressed Portfolio Management at PIMCO ▪ Former Managing Principal at MHR Fund Management LLC ▪ Previously served as Member of the Event Driven Strategies Group at Highbridge Capital Management Monocle Acquisition Corporation ▪ More than 30 years of experience in aircraft leasing, finance, maintenance, supply chain services and airline operations with an extensive network of industry relationships ▪ Co - Founded AerSale in 2008 ▪ Co - Founder and former CEO of AeroTurbine, Inc., before selling the company in 2006 to AerCap (NYSE:AER) Nicolas Finazzo Co - Founder, Chairman & CEO AerSale Corp. ▪ 20 years of relevant industry experience in accounting and finance ▪ Joined AerSale in 2015 as Vice President of Finance & Corporate Controller ▪ Previously served as Senior Director of Corporate Accounting for Florida Power & Light, the regulated utility of NextEra Energy, Inc (NYSE:NEE) ▪ Formerly served as Controller during the IPO of NextEra Energy Partners, LP (NYSE:NEP) Martin Garmendia Chief Financial Officer ▪ Over 30 years of experience in aircraft engine sales, leasing and MRO services ▪ Co - Founded AerSale in 2008 ▪ Co - Founder and former COO of AeroTurbine, Inc., before selling the company in 2006 to AerCap (NYSE:AER) ▪ Manager of Powerplant and Warranty Administration for Braniff Airways ▪ Director of Engine Maintenance Sales for Greenwich Air Services (acquired by GE Engine Services) Robert Nichols Co - Founder, Executive Vice Chairman & President

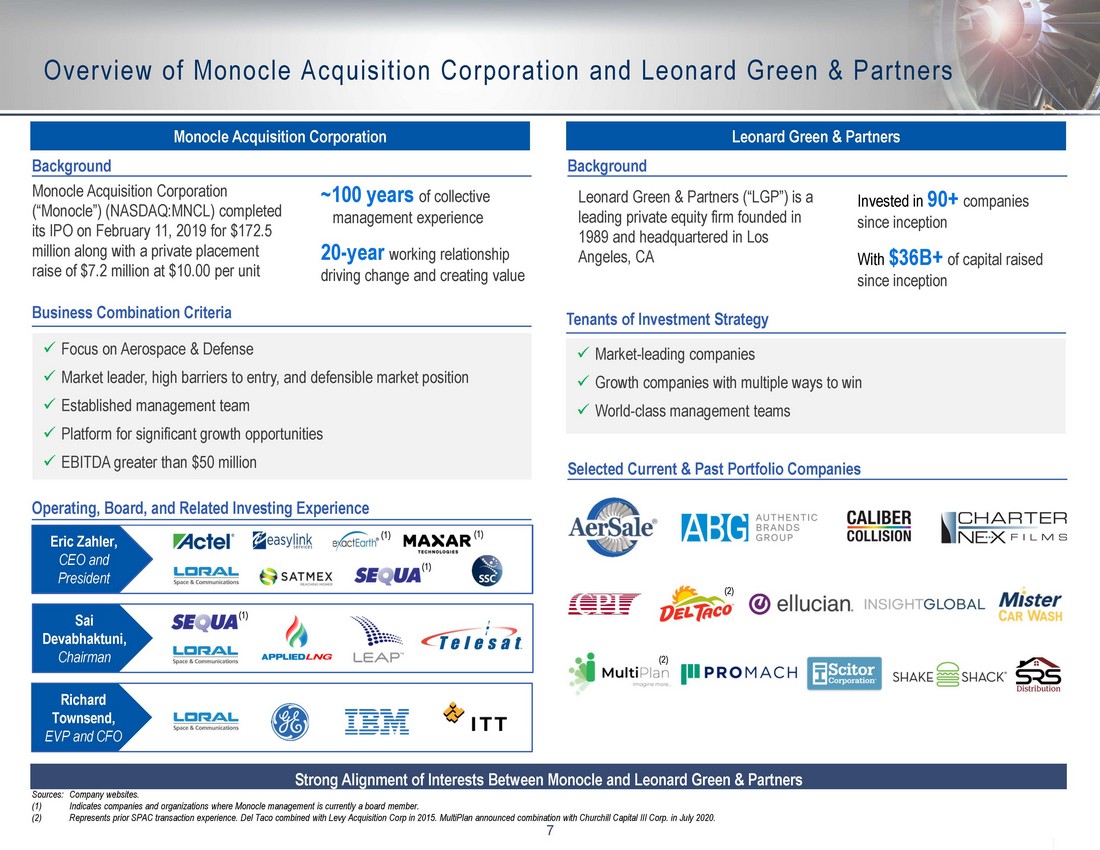

7 Overview of Monocle Acquisition Corporation and Leonard Green & Partners Monocle Acquisition Corporation (“Monocle”) (NASDAQ:MNCL) completed its IPO on February 11, 2019 for $172.5 million along with a private placement raise of $7.2 million at $10.00 per unit Background Sources: Company websites. (1) Indicates companies and organizations where Monocle management is currently a board member. (2) Represents prior SPAC transaction experience. Del Taco combined with Levy Acquisition Corp in 2015. MultiPlan announced combi nat ion with Churchill Capital III Corp. in July 2020. Monocle Acquisition Corporation Eric Zahler, CEO and President Operating, Board, and Related Investing Experience (1) (1) (1) Richard Townsend, EVP and CFO Sai Devabhaktuni, Chairman (1) x Focus on Aerospace & Defense x Market leader, high barriers to entry, and defensible market position x Established management team x Platform for significant growth opportunities x EBITDA greater than $50 million Business Combination Criteria ~100 years of collective management experience 20 - year working relationship driving change and creating value Strong Alignment of Interests Between Monocle and Leonard Green & Partners Leonard Green & Partners Leonard Green & Partners (“LGP”) is a leading private equity firm founded in 1989 and headquartered in Los Angeles, CA Background Invested in 90+ companies since inception With $36B+ of capital raised since inception Selected Current & Past Portfolio Companies x Market - leading companies x Growth companies with multiple ways to win x World - class management teams Tenants of Investment Strategy (2) (2)

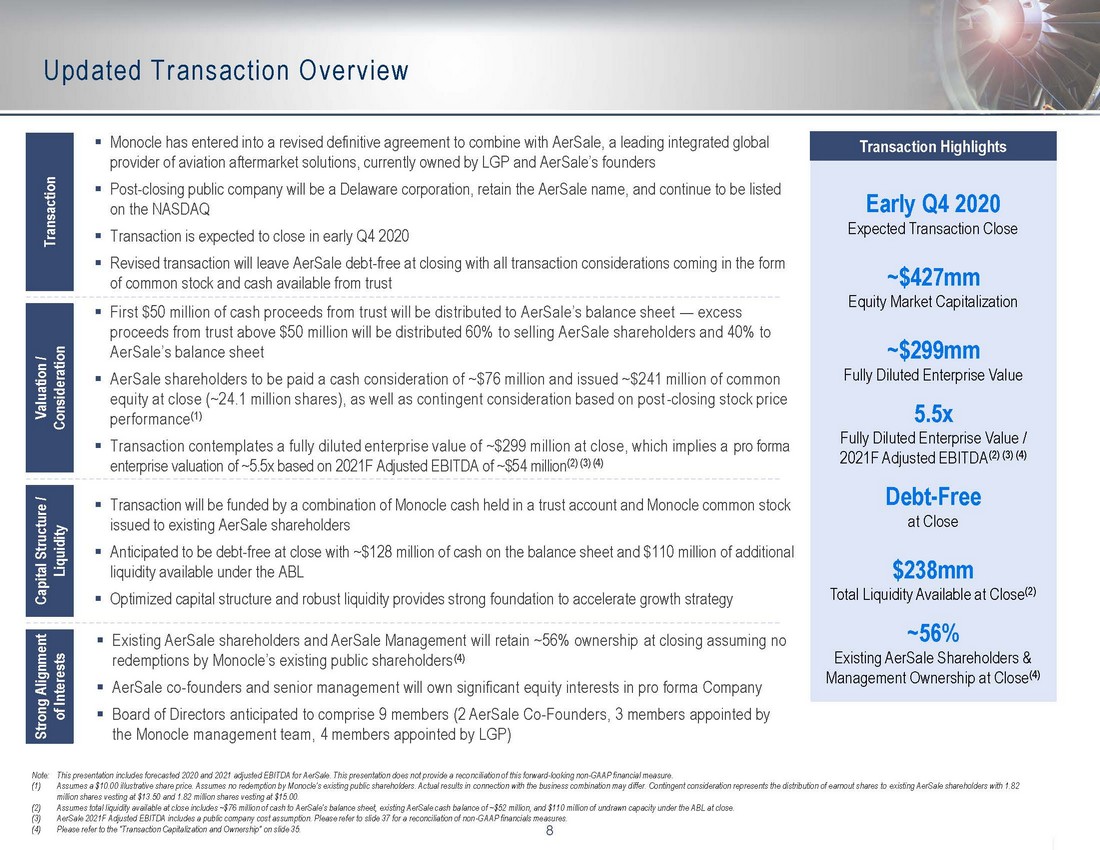

8 Updated Transaction Overview Note: This presentation includes forecasted 2020 and 2021 adjusted EBITDA for AerSale. This presentation does not provide a reco nciliation of this forward - looking non - GAAP financial measure. (1) Assumes a $10.00 illustrative share price. Assumes no redemption by Monocle’s existing public shareholders. Actual results in co nnection with the business combination may differ. Contingent consideration represents the distribution of earnout shares to ex isting AerSale shareholders with 1.5 million shares vesting at $13.50 and 1.5 million shares vesting at $15.00. (2) Assumes total liquidity available at close includes ~$76 million of cash to AerSale’s balance sheet, existing AerSale cash ba lan ce of ~$52 million, and $110 million of undrawn capacity under the ABL at close. (3) AerSale 2021F Adjusted EBITDA includes a public company cost assumption. Please refer to slide 37 for a reconciliation of non - GA AP financials measures. (4) Please refer to the “Transaction Capitalization and Ownership” on slide 35. Valuation / Consideration ▪ First $50 million of cash proceeds from trust will be distributed to AerSale’s balance sheet — excess proceeds from trust above $50 million will be distributed 60% to selling AerSale shareholders and 40% to AerSale’s balance sheet ▪ AerSale shareholders to be paid a cash consideration of ~$76 million and issued ~$239 million of common equity at close (~23.9 million shares), as well as contingent consideration based on post - closing stock price performance (1) ▪ Transaction contemplates a fully diluted enterprise value of ~$299 million at close, which implies a pro forma enterprise valuation of ~5.5x based on 2021F Adjusted EBITDA of ~$54 million (2) (3) (4) Capital Structure / Liquidity ▪ Transaction will be funded by a combination of Monocle cash held in a trust account and Monocle common stock issued to existing AerSale shareholders ▪ Anticipated to be debt - free at close with ~$128 million of cash on the balance sheet and $110 million of additional liquidity available under the ABL ▪ Optimized capital structure and robust liquidity provides strong foundation to accelerate growth strategy Strong Alignment of Interests ▪ Existing AerSale shareholders and AerSale Management will retain ~56% ownership at closing assuming no redemptions by Monocle’s existing public shareholders (4) ▪ AerSale co - founders and senior management will own significant equity interests in pro forma Company ▪ Board of Directors anticipated to comprise 9 members (2 AerSale Co - Founders, 3 members appointed by the Monocle management team, 4 members appointed by LGP) Transaction ▪ Monocle has entered into a revised definitive agreement to combine with AerSale, a leading integrated global provider of aviation aftermarket solutions, currently owned by LGP and AerSale’s founders ▪ Post - closing public company will be a Delaware corporation, retain the AerSale name, and continue to be listed on the NASDAQ ▪ Transaction is expected to close in Q3 / Q4 2020 ▪ Revised transaction will leave AerSale debt - free at closing with all transaction considerations coming in the form of common stock and cash available from trust Early Q4 2020 Expected Transaction Close ~$427mm Equity Market Capitalization 5.5x Fully Diluted Enterprise Value / 2021F Adjusted EBITDA (2) (3) (4) Transaction Highlights Debt - Free at Close ~56% Existing AerSale Shareholders & Management Ownership at Close (4) $238mm Total Liquidity Available at Close (2) ~$299mm Fully Diluted Enterprise Value

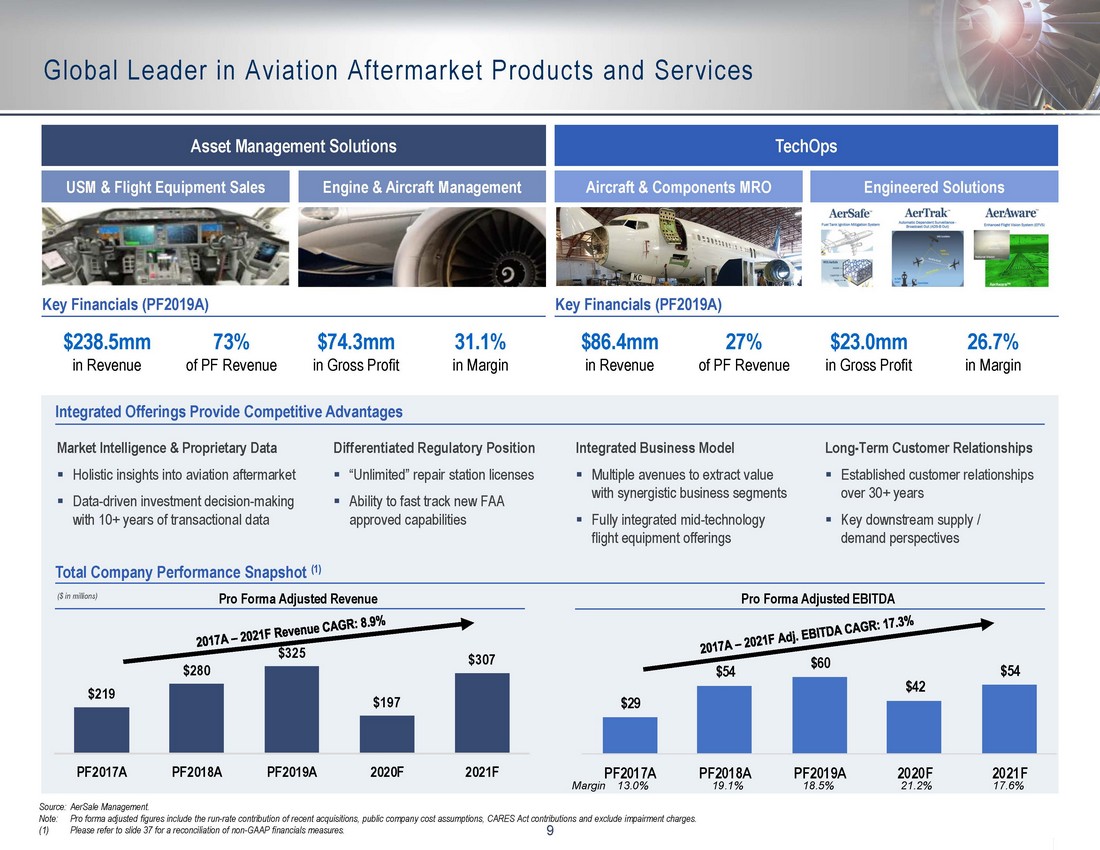

9 Global Leader in Aviation Aftermarket Products and Services Source: AerSale Management. Note: Pro forma adjusted figures include the run - rate contribution of recent acquisitions, public company cost assumptions, CARE S Act contributions and exclude impairment charges. (1) Please refer to slide 37 for a reconciliation of non - GAAP financials measures. Asset Management Solutions TechOps USM & Flight Equipment Sales Engine & Aircraft Management Aircraft & Components MRO Engineered Solutions Key Financials (PF2019A) $238.5mm in Revenue $74.3mm in Gross Profit 31.1% in Margin 73% of PF Revenue Key Financials (PF2019A) $86.4mm in Revenue $23.0mm in Gross Profit 26.7% in Margin 27% of PF Revenue Total Company Performance Snapshot (1) Pro Forma Adjusted Revenue ($ in millions) Pro Forma Adjusted EBITDA Margin 19.1% 18.5% 13.0% 21.2% Integrated Offerings Provide Competitive Advantages Market Intelligence & Proprietary Data ▪ Holistic insights into aviation aftermarket ▪ Data - driven investment decision - making with 10+ years of transactional data Integrated Business Model ▪ Multiple avenues to extract value with synergistic business segments ▪ Fully integrated mid - technology flight equipment offerings Differentiated Regulatory Position ▪ “Unlimited” repair station licenses ▪ Ability to fast track new FAA approved capabilities Long - Term Customer Relationships ▪ Established customer relationships over 30+ years ▪ Key downstream supply / demand perspectives 17.6% $219 $280 $325 $197 $307 PF2017A PF2018A PF2019A 2020F 2021F $29 $54 $60 $42 $54 PF2017A PF2018A PF2019A 2020F 2021F

10 7 Business combination at an attractive valuation relative to public commercial aerospace peers 4 Multiple levers for sustained organic growth across existing and new business lines 6 Proven leadership team with deep industry expertise across multiple aviation business cycles 2 Differentiated business model designed to maximize return on investment and sustain cash flow across cycles 3 Long - standing relationships across the value chain to support procurement and monetization of assets 5 Scalable platform for growth through M&A, with a demonstrated ability to acquire and integrate businesses 1 Well - positioned to capitalize on commercial aviation market dislocation with strong, debt - free balance sheet AerSale Investment Highlights

Section II Business Overview & Growth Opportunities

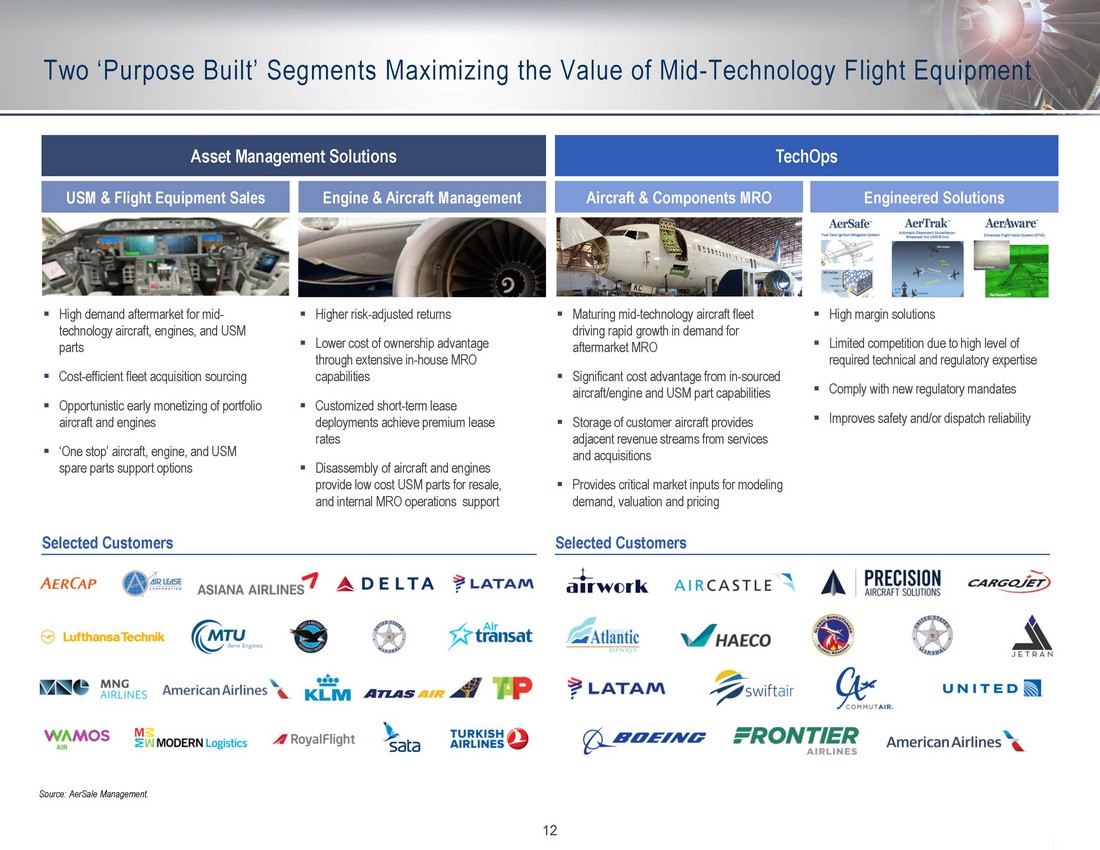

12 Two ‘Purpose Built’ Segments Maximizing the Value of Mid - Technology Flight Equipment ▪ High demand aftermarket for mid - technology aircraft, engines, and USM parts ▪ Cost - efficient fleet acquisition sourcing ▪ Opportunistic early monetizing of portfolio aircraft and engines ▪ ‘One stop’ aircraft, engine, and USM spare parts support options Source: AerSale Management. Asset Management Solutions TechOps USM & Flight Equipment Sales Engine & Aircraft Management Aircraft & Components MRO Engineered Solutions Selected Customers ▪ Higher risk - adjusted returns ▪ Lower cost of ownership advantage through extensive in - house MRO capabilities ▪ Customized short - term lease deployments achieve premium lease rates ▪ Disassembly of aircraft and engines provide low cost USM parts for resale, and internal MRO operations support ▪ Maturing mid - technology aircraft fleet driving rapid growth in demand for aftermarket MRO ▪ Significant cost advantage from in - sourced aircraft/engine and USM part capabilities ▪ Storage of customer aircraft provides adjacent revenue streams from services and acquisitions ▪ Provides critical market inputs for modeling demand, valuation and pricing ▪ High margin solutions ▪ Limited competition due to high level of required technical and regulatory expertise ▪ Comply with new regulatory mandates ▪ Improves safety and/or dispatch reliability Selected Customers

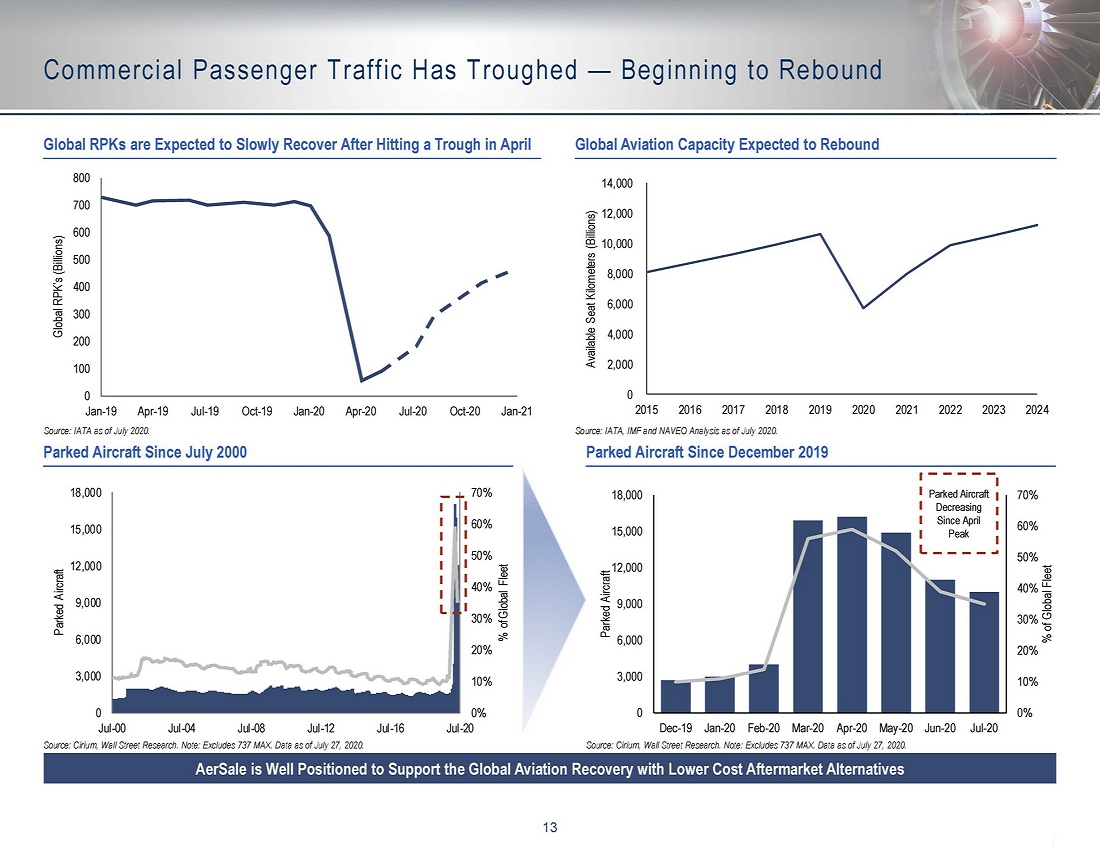

13 0% 10% 20% 30% 40% 50% 60% 70% 0 3,000 6,000 9,000 12,000 15,000 18,000 Jul-00 Jul-04 Jul-08 Jul-12 Jul-16 Jul-20 % of Global Fleet Parked Aircraft AerSale is Well Positioned to Support the Global Aviation Recovery with Lower Cost Aftermarket Alternatives Parked Aircraft Since July 2000 Parked Aircraft Since December 2019 Source: Cirium, Wall Street Research. Note: Excludes 737 MAX. Data as of July 27, 2020. Source: Cirium, Wall Street Research. Note: Excludes 737 MAX. Data as of July 27, 2020. 0% 10% 20% 30% 40% 50% 60% 70% 0 3,000 6,000 9,000 12,000 15,000 18,000 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 % of Global Fleet Parked Aircraft Parked Aircraft Decreasing Since April Peak Commercial Passenger Traffic Has Troughed — Beginning to Rebound Source: IATA as of July 2020. Global Aviation Capacity Expected to Rebound Global RPKs are Expected to Slowly Recover After Hitting a Trough in April 0 100 200 300 400 500 600 700 800 Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Global RPK’s (Billions) Source: IATA, IMF and NAVEO Analysis as of July 2020. 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 Available Seat Kilometers (Billions)

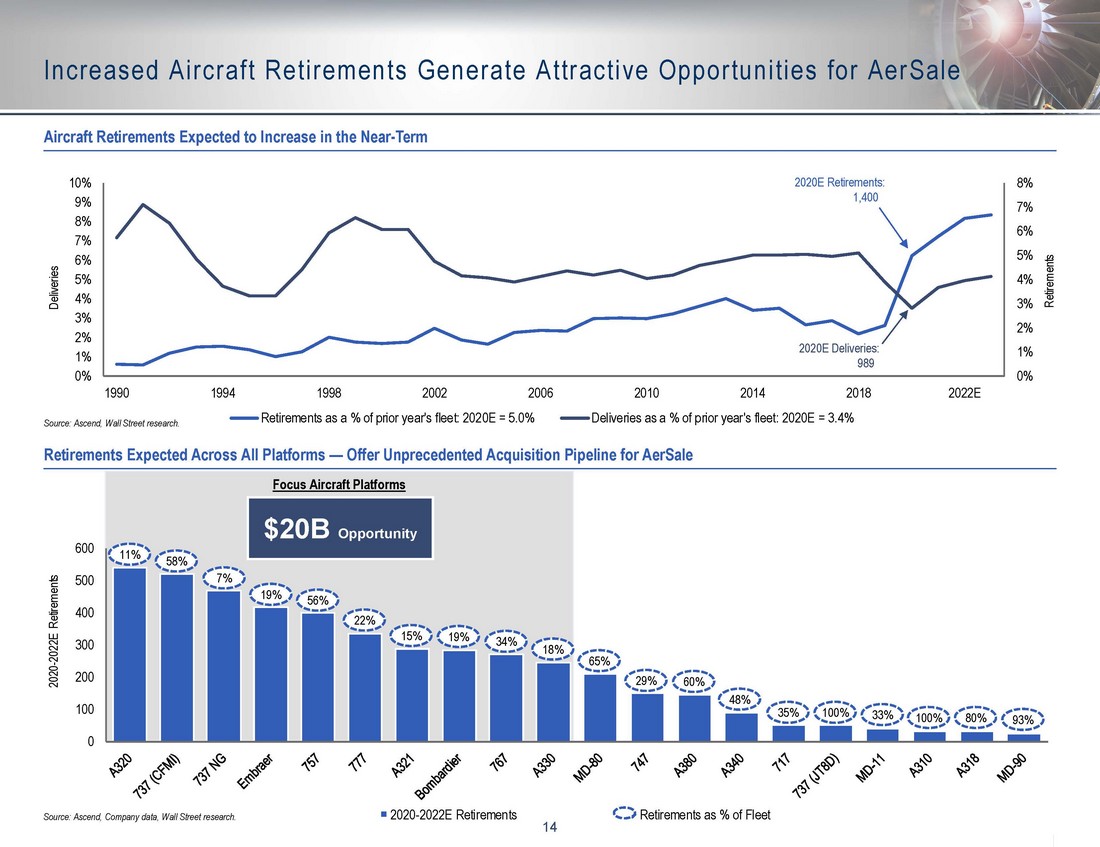

14 Increased Aircraft Retirements Generate Attractive Opportunities for AerSale Focus Aircraft Platforms 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1990 1994 1998 2002 2006 2010 2014 2018 2022E 0% 1% 2% 3% 4% 5% 6% 7% 8% Deliveries Retirements Retirements as a % of prior year's fleet: 2020E = 5.0% Deliveries as a % of prior year's fleet: 2020E = 3.4% Source: Ascend, Wall Street research. Aircraft Retirements Expected to Increase in the Near - Term 2020E Retirements: 1,400 2020E Deliveries: 989 Retirements Expected Across All Platforms — Offer Unprecedented Acquisition Pipeline for AerSale Source: Ascend, Company data, Wall Street research. $20B Opportunity 11% 58% 7% 19% 56% 22% 15% 19% 34% 18% 65% 29% 60% 48% 35% 100% 33% 100% 80% 93% 0 100 200 300 400 500 600 700 800 2020 - 2022E Retirements 2020-2022E Retirements Retirements as % of Fleet 0 100 200 300 400 500 600 2020 - 2022E Retirements 11% 58% 7% 19% 56% 22% 15% 19% 34% 18% 65% 29% 60% 48% 35% 100% 33% 100% 80% 93%

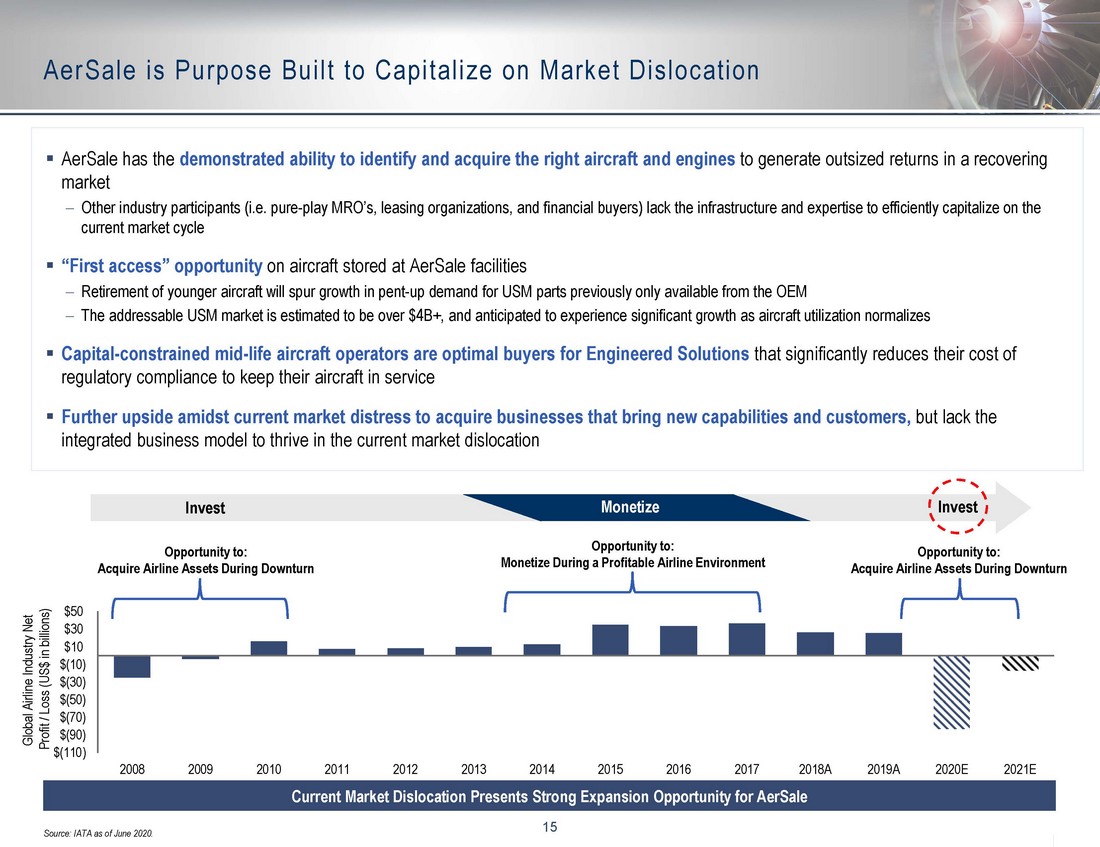

15 AerSale is Purpose Built to Capitalize on Market Dislocation Current Market Dislocation Presents Strong Expansion Opportunity for AerSale ▪ AerSale has the demonstrated ability to identify and acquire the right aircraft and engines to generate outsized returns in a recovering market Other industry participants (i.e. pure - play MRO’s, leasing organizations, and financial buyers) lack the infrastructure and expe rtise to efficiently capitalize on the current market cycle ▪ “First access” opportunity on aircraft stored at AerSale facilities Retirement of younger aircraft will spur growth in pent - up demand for USM parts previously only available from the OEM The addressable USM market is estimated to be over $4B+, and anticipated to experience significant growth as aircraft utiliza tio n normalizes ▪ Capital - constrained mid - life aircraft operators are optimal buyers for Engineered Solutions that significantly reduces their cost of regulatory compliance to keep their aircraft in service ▪ Further upside amidst current market distress to acquire businesses that bring new capabilities and customers, but lack the integrated business model to thrive in the current market dislocation Source: IATA as of June 2020. Opportunity to: Acquire Airline Assets During Downturn Invest Invest Sell Opportunity to: Acquire Airline Assets During Downturn Opportunity to: Monetize During a Profitable Airline Environment Monetize Global Airline Industry Net Profit / Loss (US$ in billions) $(110) $(90) $(70) $(50) $(30) $(10) $10 $30 $50 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018A 2019A 2020E 2021E

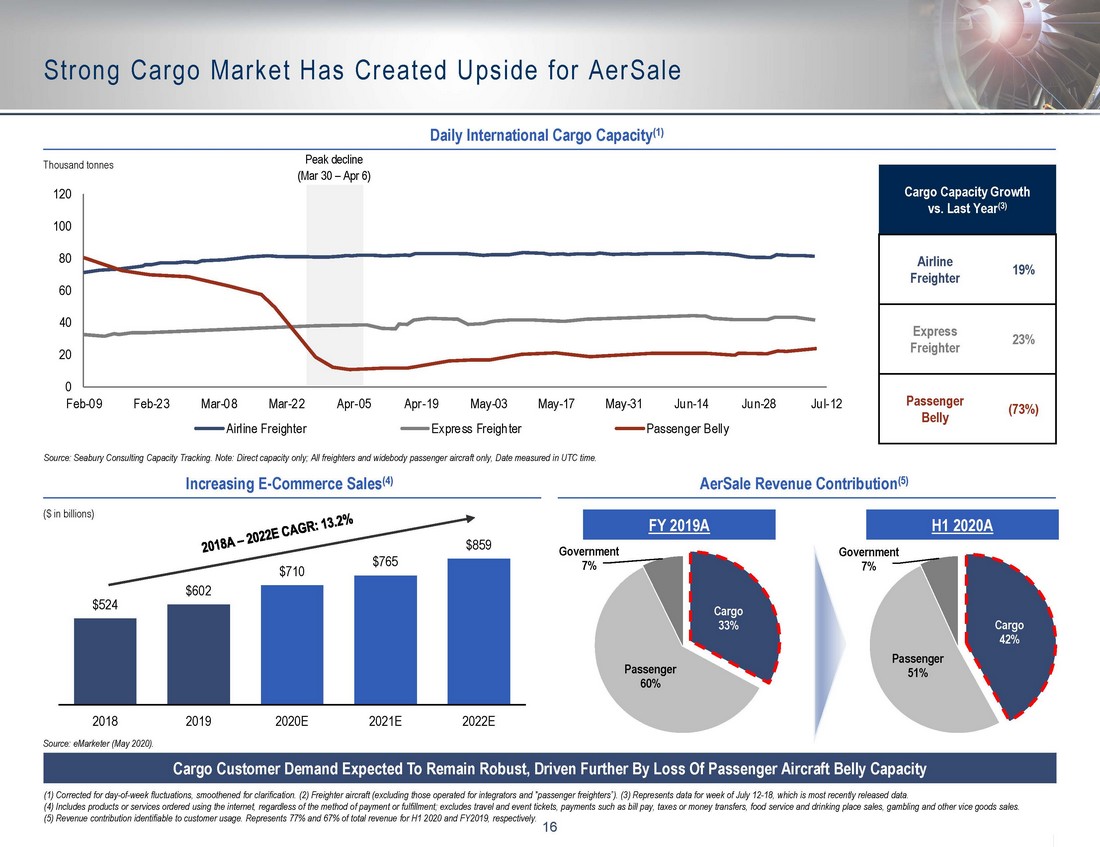

16 0 20 40 60 80 100 120 Feb-09 Feb-23 Mar-08 Mar-22 Apr-05 Apr-19 May-03 May-17 May-31 Jun-14 Jun-28 Jul-12 Airline Freighter Express Freighter Passenger Belly Strong Cargo Market Has Created Upside for AerSale (1) Corrected for day - of - week fluctuations, smoothened for clarification. (2) Freighter aircraft (excluding those operated for i ntegrators and "passenger freighters”). (3) Represents data for week of July 12 - 18, which is most recently released data. (4) Includes products or services ordered using the internet, regardless of the method of payment or fulfillment; excludes tr ave l and event tickets, payments such as bill pay, taxes or money transfers, food service and drinking place sales, gambling and ot her vice goods sales. (5) Revenue contribution identifiable to customer usage. Represents 77% and 67% of total revenue for H1 2020 and FY2019, resp ect ively. Peak decline (Mar 30 – Apr 6) Cargo Customer Demand Expected To Remain Robust, Driven Further By Loss Of Passenger Aircraft Belly Capacity Increasing E - Commerce Sales (4) $524 $602 $710 $765 $859 2018 2019 2020E 2021E 2022E Source: eMarketer (May 2020). AerSale Revenue Contribution (5) Cargo 33% Passenger 60% Government 7% Cargo Capacity Growth vs. Last Year (3) Airline Freighter 19% Express Freighter 23% Passenger Belly (73%) Daily International Cargo Capacity (1) Source: Seabury Consulting Capacity Tracking. Note: Direct capacity only; All freighters and widebody passenger aircraft only , D ate measured in UTC time. Thousand tonnes ($ in billions) Cargo 42% Passenger 51% Government 7% H1 2020A FY 2019A

17 Significant Opportunity to Capitalize on Current Market Conditions USM Ripe for Recovery 1 ▪ As an attractive alternative to expensive “new” replacement parts , USM is well positioned to rapidly expand as air travel normalizes ▪ Required inspections to bring thousands of mid - life aircraft / engines out of preservation for return to service, is set to drive significant growth in USM consumption in a recovering market Leasing Business Positioned to Expand 2 ▪ Unprecedented buying window has opened , which will foster high - margin leasing growth as increasing number of aircraft return to service ▪ “Green time” engines to be in high demand by Airlines as alternative to expensive engine shop visit restorations ▪ Growing demand for lease engines amid required engine inspections , as stored aircraft return to service Ideal Conditions for Expansion 5 ▪ Most established mid - life aircraft participants over - extended amid a pre - COVID - 19 overheated market ▪ Distressed competitive landscape ideal for capturing assets, infrastructure and talent MRO and Aircraft Storage 3 ▪ Record demand for aircraft storage has AerSale parking areas loaded to near capacity, with additional parking surface area currently under construction ▪ Record level captive audience for future aircraft activations, modifications, transitions and acquisitions Growing Dedicated Freighter Market 4 ▪ Increased e - commerce activity in combination with decreased ‘belly cargo’ capacity from passenger flight reductions, are driving current surge in demand for dedicated freighters and passenger - to - freighter conversion services ▪ AerSale in discussions with freighter operators, aircraft OEMs, and cargo door STC holders to increase AerSale’s aircraft conversion capacity in combination with integrated MRO support services Robust Financial Position 6 ▪ A diversified business model has enabled AerSale to weather the storm and r emain cash flow positive every month during the pandemic ▪ Unleveraged balance sheet provides tremendous opportunity

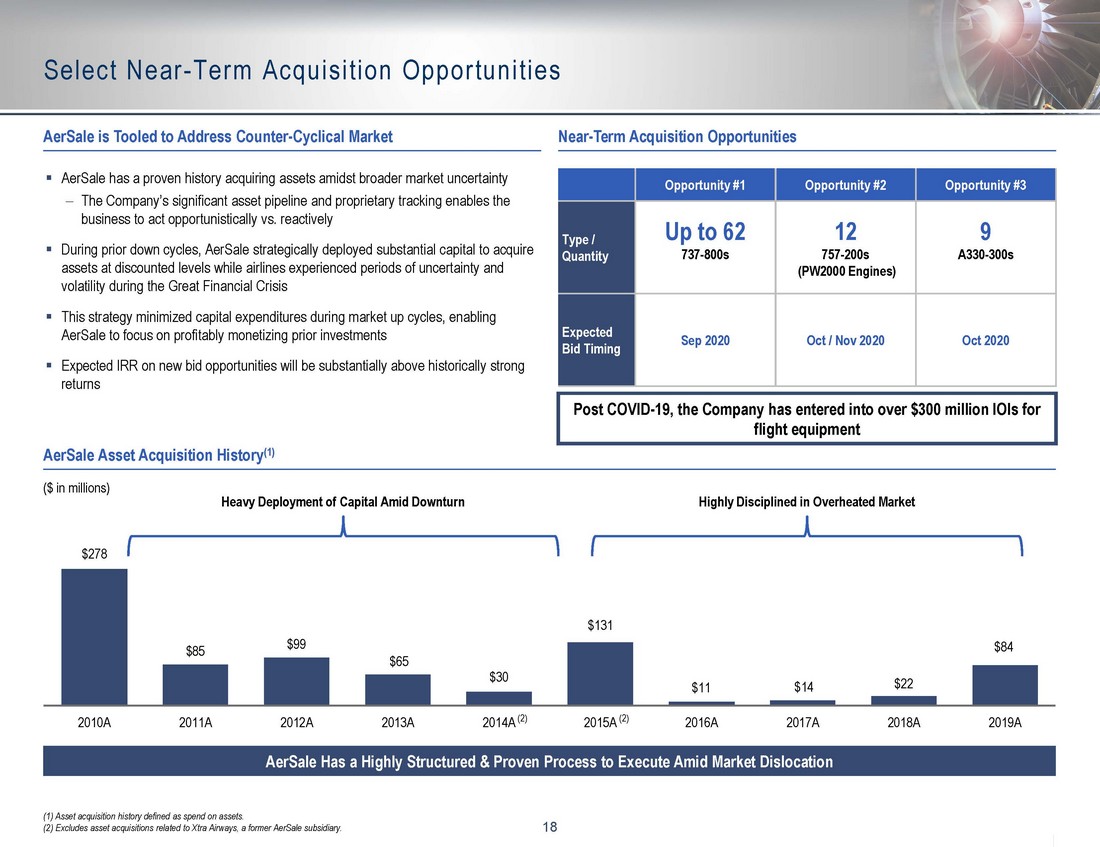

18 Select Near - Term Acquisition Opportunities Opportunity #1 Opportunity #2 Opportunity #3 Type / Quantity Up to 62 737 - 800s 12 757 - 200s (PW2000 Engines) 9 A330 - 300s Expected Bid Timing Sep 2020 Oct / Nov 2020 Oct 2020 AerSale Asset Acquisition History (1) ($ in millions) AerSale Has a Highly Structured & Proven Process to Execute Amid Market Dislocation (1) Asset acquisition history defined as spend on assets. (2) Excludes asset acquisitions related to Xtra Airways, a former AerSale subsidiary. (2) (2) Near - Term Acquisition Opportunities ▪ AerSale has a proven history acquiring assets amidst broader market uncertainty The Company’s significant asset pipeline and proprietary tracking enables the business to act opportunistically vs. reactively ▪ During prior down cycles, AerSale strategically deployed substantial capital to acquire assets at discounted levels while airlines experienced periods of uncertainty and volatility during the Great Financial Crisis ▪ This strategy minimized capital expenditures during market up cycles, enabling AerSale to focus on profitably monetizing prior investments ▪ Expected IRR on new bid opportunities will be substantially above historically strong returns AerSale is Tooled to Address Counter - Cyclical Market Heavy Deployment of Capital Amid Downturn Highly Disciplined in Overheated Market $278 $85 $99 $65 $30 $131 $11 $14 $22 $84 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017A 2018A 2019A Post COVID - 19, the Company has entered into over $300 million IOIs for flight equipment

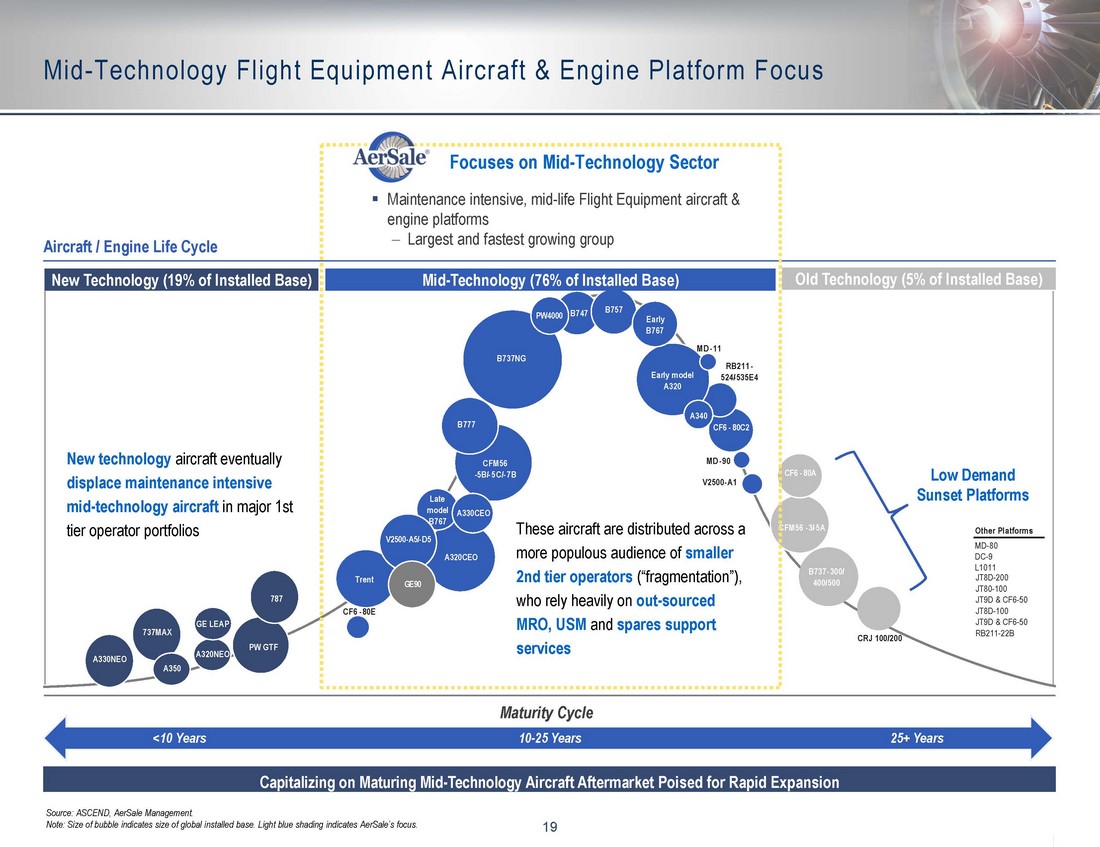

19 B737NG Mid - Technology Flight Equipment Aircraft & Engine Platform Focus Ear l y mode l A 320 A330CEO M D - 9 0 CRJ 100/2 0 0 M D - 1 1 T rent B757 C F 6 - 80 C 2 V250 0 - A 1 CFM 5 6 - 3 / - 5 A B73 7 - 300/ 400/5 00 A 340 A330NEO PW 4000 A320CEO CFM 5 6 - 5 B / - 5 C / - 7 B V 250 0 - A 5 / - D 5 C F 6 - 80E B777 Late m odel B767 MD - 80 DC - 9 L1011 JT8D - 200 JT80 - 100 JT9D & CF6 - 50 JT8D - 100 JT9D & CF6 - 50 RB211 - 22B New Technology (19% of Installed Base) Mid - Technology (76% of Installed Base) Old Technology (5% of Installed Base) RB2 1 1 - 524 / - 5 35E4 Source: ASCEND, AerSale Management. Note: Size of bubble indicates size of global installed base. Light blue shading indicates AerSale’s focus. Aircraft / Engine Life Cycle 737MAX A350 A320NEO GE LEAP PW GTF 787 Ear l y B767 C F 6 - 80 A B747 Focuses on Mid - Technology Sector GE90 Other Platforms New technology aircraft eventually displace maintenance intensive mid - technology aircraft in major 1st tier operator portfolios These aircraft are distributed across a more populous audience of smaller 2nd tier operators (“fragmentation”), who rely heavily on out - sourced MRO, USM and spares support services ▪ Maintenance intensive, mid - life Flight Equipment aircraft & engine platforms Largest and fastest growing group Maturity Cycle 10 - 25 Years 25+ Years <10 Years Capitalizing on Maturing Mid - Technology Aircraft Aftermarket Poised for Rapid Expansion Low Demand Sunset Platforms

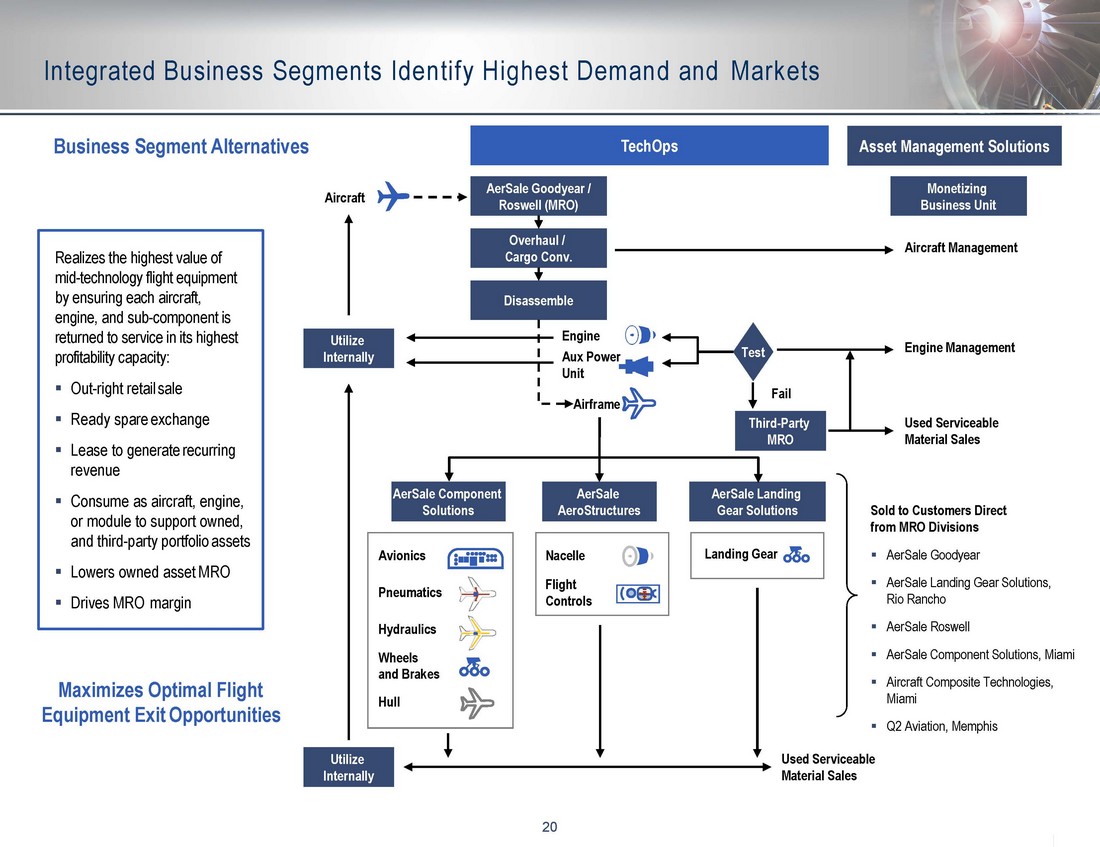

20 Integrated Business Segments Identify Highest Demand and Markets Business Segment Alternatives Realizes the highest value of mid - technology flight equipment by ensuring each aircraft, engine, and sub - component is returned to service in it s highest profitability capacity: ▪ Out - right retail sale ▪ Ready spare exchange ▪ Lease to generate recurring revenue ▪ Consume as aircraft, engine, or module to support owned, and third - party portfolio assets ▪ Lowers owned asset MRO ▪ Drives MRO margin Maximizes Optimal Flight Equipment Exit Opportunities Aircraft Airframe Utilize Internally Utilize Internally AerSale Component Solutions AerSale Landing Gear Solutions Third - Party MRO AerSale Goodyear / Roswell (MRO) Overhaul / Cargo Conv. Disassemble Engine Aux Power Unit Aircraft Management Engine Management Used Serviceable Material Sales Test Fail Sold to Customers Direct from MRO Divisions ▪ AerSale Goodyear ▪ AerSale Landing Gear Solutions, Rio Rancho ▪ AerSale Roswell ▪ AerSale Component Solutions, Miami ▪ Aircraft Composite Technologies, Miami ▪ Q2 Aviation, Memphis Monetizing Business Unit Avionics Pneumatics Hydraulics Wheels and Brakes Hull Nacelle Flight Controls Used Serviceable Material Sales AerSale AeroStructures TechOps Asset Management Solutions Landing Gear

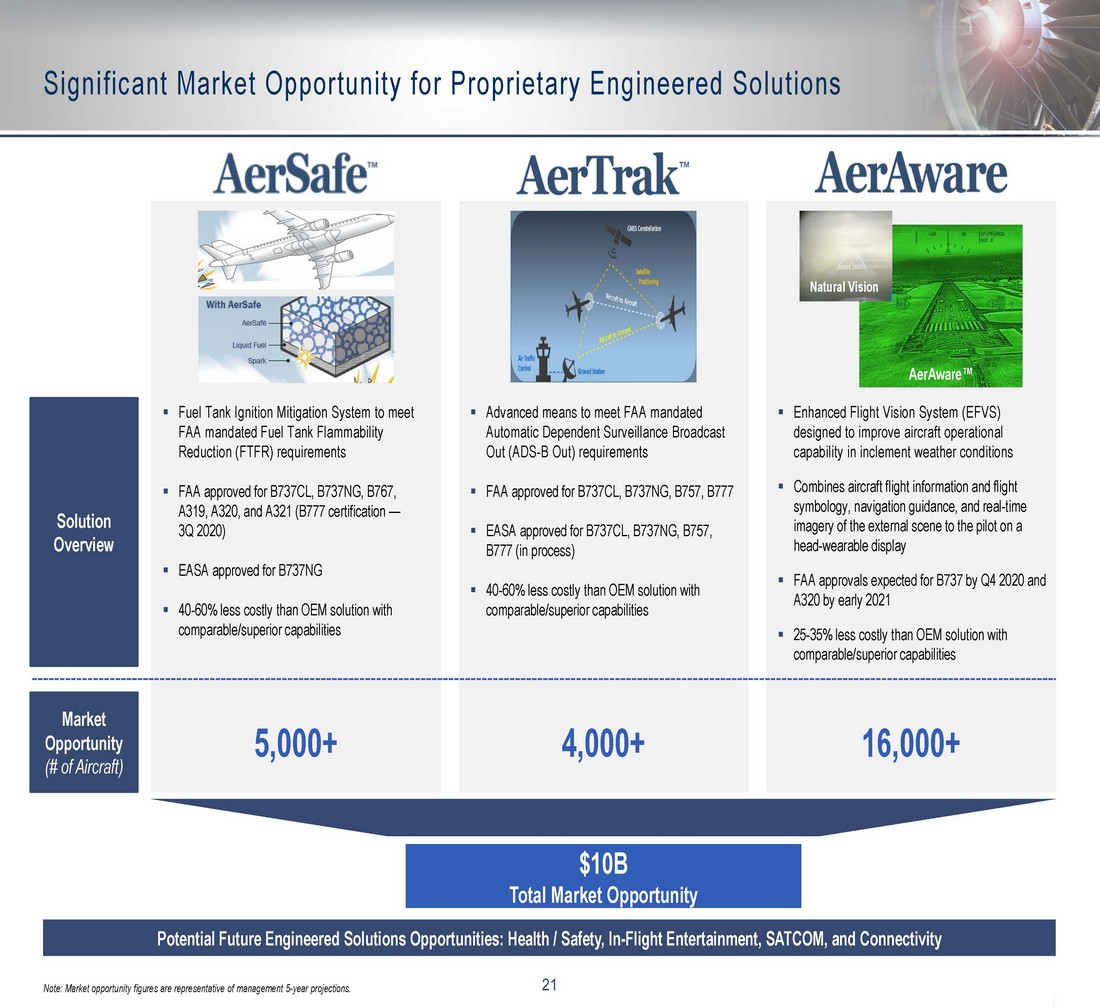

21 Significant Market Opportunity for Proprietary Engineered Solutions $10B Total Market Opportunity 5,000+ 4,000+ 16,000+ Market Opportunity (# of Aircraft) ▪ Fuel Tank Ignition Mitigation System to meet FAA mandated Fuel Tank Flammability Reduction (FTFR) requirements ▪ FAA approved for B737CL, B737NG, B767, A319, A320, and A321 (B777 certification — 3Q 2020) ▪ EASA approved for B737NG ▪ 40 - 60% less costly than OEM solution with comparable/superior capabilities ▪ Advanced means to meet FAA mandated Automatic Dependent Surveillance Broadcast Out (ADS - B Out) requirements ▪ FAA approved for B737CL, B737NG, B757, B777 ▪ EASA approved for B737CL, B737NG, B757, B777 (in process) ▪ 40 - 60% less costly than OEM solution with comparable/superior capabilities ▪ Enhanced Flight Vision System (EFVS) designed to improve aircraft operational capability in inclement weather conditions ▪ Combines aircraft flight information and flight symbology, navigation guidance, and real - time imagery of the external scene to the pilot on a head - wearable display ▪ FAA approvals expected for B737 by Q4 2020 and A320 by early 2021 ▪ 25 - 35% less costly than OEM solution with comparable/superior capabilities Solution Overview Potential Future Engineered Solutions Opportunities: Health / Safety, In - Flight Entertainment, SATCOM, and Connectivity Note: Market opportunity figures are representative of management 5 - year projections. Natural Vision AerAware™

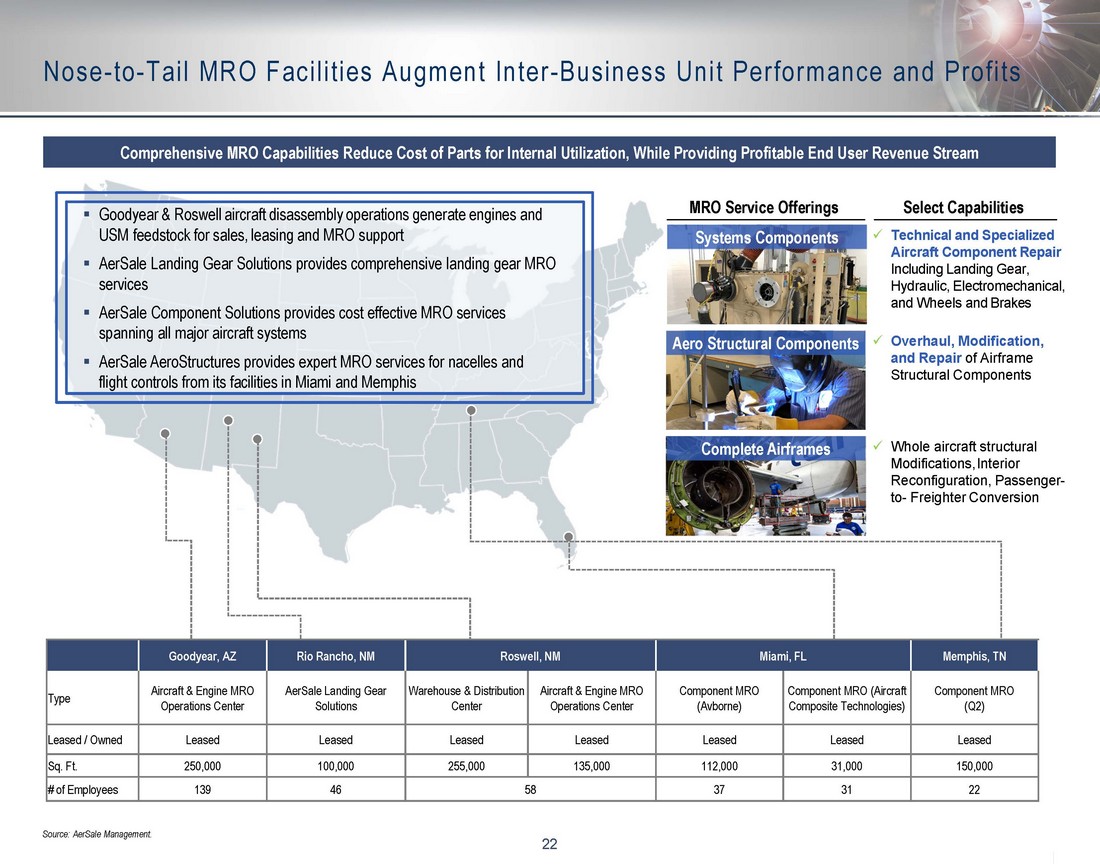

22 Nose - to - Tail MRO Facilities Augment Inter - Business Unit Performance and Profits Select Capabilities Comprehensive MRO Capabilities Reduce Cost of Parts for Internal Utilization, While Providing Profitable End User Revenue Str eam MRO Service Offerings Source: AerSale Management. Systems Components Aero Structural Components Complete Airframes ▪ Goodyear & Roswell aircraft disassembly operations generate engines and USM feedstock for sales, leasing and MRO support ▪ AerSale Landing Gear Solutions provides comprehensive landing gear MRO services ▪ AerSale Component Solutions provides cost effective MRO services spanning all major aircraft systems ▪ AerSale AeroStructures provides expert MRO services for nacelles and flight controls from its facilities in Miami and Memphis x Overhaul, Modification, and Repair of Airframe Structural Components x Whole aircraft s tructural Modifications, Interior Reconfiguration, Passenger - to - Freighter Conversion x Technical and Specialized Aircraft Component Repair Including Landing Gear, Hydraulic, Electromechanical, and Wheels and Brakes Goodyear, AZ Rio Rancho, NM Roswell, NM Miami, FL Memphis, TN Type Aircraft & Engine MRO Operations Center AerSale Landing Gear Solutions Warehouse & Distribution Center Aircraft & Engine MRO Operations Center Component MRO (Avborne) Component MRO (Aircraft Composite Technologies) Component MRO (Q2) Leased / Owned Leased Leased Leased Leased Leased Leased Leased Sq. Ft. 250,000 100,000 255,000 135,000 112,000 31,000 150,000 # of Employees 139 46 58 37 31 22

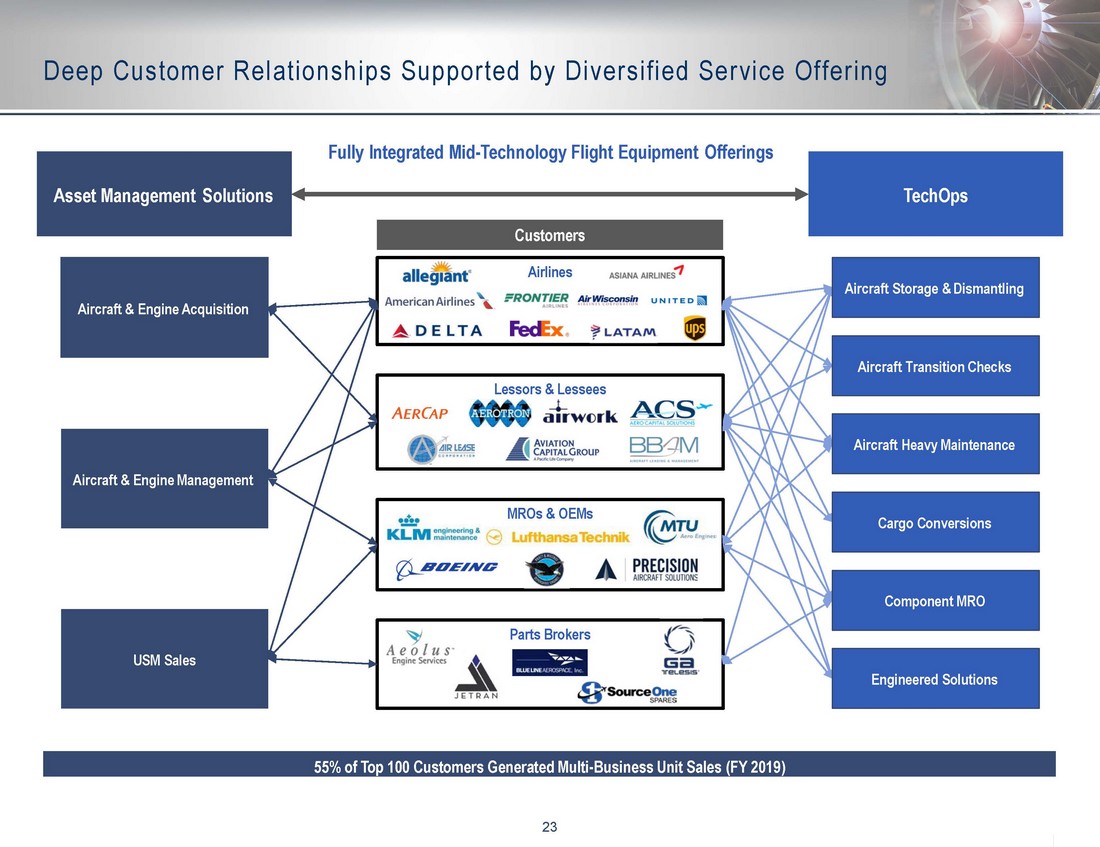

23 Deep Customer Relationships Supported by Diversified Service Offering 55 % of Top 100 Customers Generated Multi - Business Unit Sales (FY 201 9 ) Asset Management Solutions Aircraft & Engine Acquisition Aircraft & Engine Management USM Sales Customers Airlines MROs & OEMs Lessors & Lessees Parts Brokers TechOps Aircraft Heavy Maintenance Aircraft Storage & Dismantling Component MRO Cargo Conversions Aircraft Transition Checks Engineered Solutions Fully Integrated Mid - Technology Flight Equipment Offerings

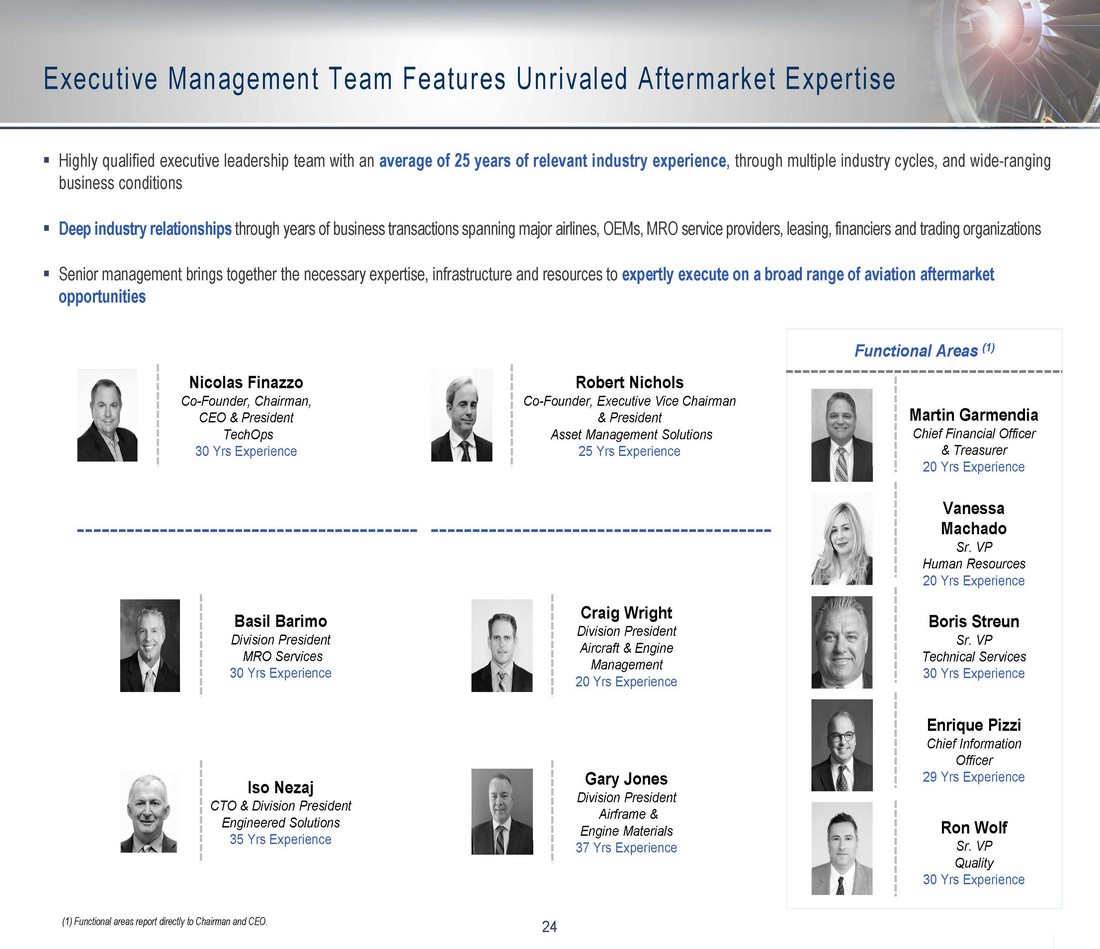

24 Executive Management Team Features Unrivaled Aftermarket Expertise ▪ Highly qualified executive leadership team with an average of 25 years of relevant industry experience , through multiple industry cycles, and wide - ranging business conditions ▪ Deep industry relationships through years of business transactions spanning major airlines, OEMs, MRO service providers, leasing, financiers and trading org anizations ▪ S enior management brings together the necessary expertise, infrastructure and resources to expertly execute on a broad range of aviation aftermarket opportunities 24 Martin Garmendia Chief Financial Officer & Treasurer 20 Yrs Experience Vanessa Machado Sr. VP Human Resources 20 Yrs Experience Functional Areas (1) Robert Nichols Co - Founder, Executive Vice Chairman & President Asset Management Solutions 25 Yrs Experience Craig Wright Division President Aircraft & Engine Management 20 Yrs Experience Nicolas Finazzo Co - Founder, Chairman, CEO & President TechOps 30 Yrs Experience Basil Barimo Division President MRO Services 30 Yrs Experience Iso Nezaj CTO & Division President Engineered Solutions 35 Yrs Experience Ron Wolf Sr. VP Quality 30 Yrs Experience (1) Functional areas report directly to Chairman and CEO. Gary Jones Division President Airframe & Engine Materials 37 Yrs Experience Enrique Pizzi Chief Information Officer 29 Yrs Experience Boris Streun Sr. VP Technical Services 30 Yrs Experience

25 Attractive Global Opportunities For Scalable Business Platform Expanded Sales to U.S. Government Agencies • Stable and increasing DoD O&M budget — ~5% CAGR from FY2016 to FY2020 • Defense sector in early stage of outsourced solutions for aging aircraft platforms • AerSale has successfully executed on numerous governmental agency awards 4 Aviation Aftermarket Trough Poised to Rebound • Unprecedented opportunity to acquire aircraft / feedstock at discounted values amid wave of aircraft retirements • Massive grounding of global fleets to drive significant surge in MRO demand as aircraft are recertified for return to service 1 Development of New High - Margin MRO Capabilities • Global MRO market will continue to grow — >3% CAGR expected through 2024 • Rapidly expanding demand for landing gear MRO capacity • Facilities and expertise in place to profitably scale AerSale’s MRO capabilities 3 Scalable Platform With Proven and Accretive M&A Strategy • Well - positioned for future acquisitions within highly fragmented aviation aftermarket industry • Focus on expanding core capabilities & solutions, expansion into adjacent categories, and penetrating new customers & markets • Long track record of successful integration 6 Development & Innovation of New Engineered Solutions Offerings • Rapidly increasing demand for significant savings on alternative products and services needed to enhance aircraft performance • High - margin proprietary repairs, modifications, and aircraft system installations that are difficult to replicate 2 Geographic Expansion of MRO Services • Initial focus is Asia Pacific Region, the largest and fastest growing aviation market region • Developing partnerships with regional MRO providers to fast - track local capabilities • Creates a regional platform for USM distribution, Engineered Solutions sales and other services • Strengthens AerSale’s brand and creates blueprint for other regions (e.g. Middle East and LatAm) 5 Source: Oliver Wyman 2018 - 2028 Global Fleet MRO Market Forecast, Department of Defense Office of the Comptroller , AerSale Management.

Section III Financial Detail & Transaction Summary

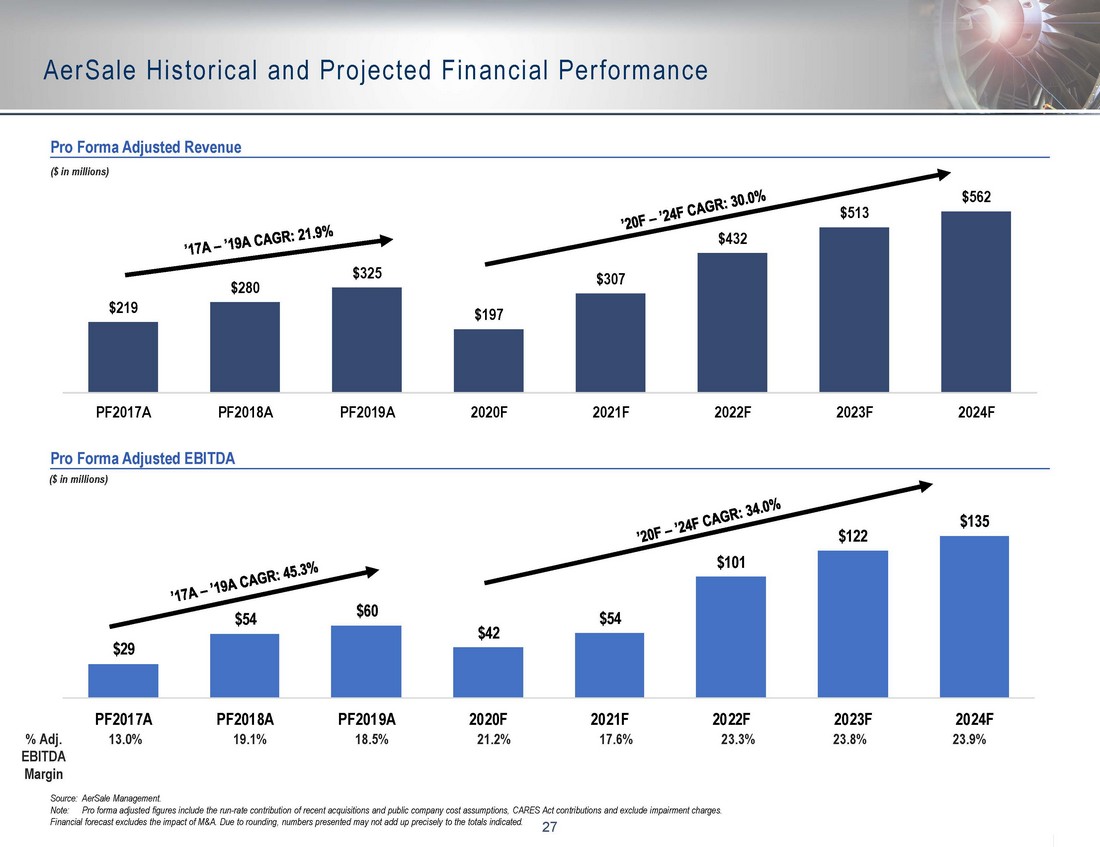

27 $29 $54 $60 $42 $54 $101 $122 $135 PF2017A PF2018A PF2019A 2020F 2021F 2022F 2023F 2024F AerSale Historical and Projected Financial Performance Source: AerSale Management. Note: Pro forma adjusted figures include the run - rate contribution of recent acquisitions and public company cost assumptions, CARES Act contributions and exclude impairment charges. Financial forecast excludes the impact of M&A. Due to rounding, numbers presented may not add up precisely to the totals indi cat ed. Pro Forma Adjusted Revenue ($ in millions) Pro Forma Adjusted EBITDA % Adj. EBITDA Margin 13.0% 19.1% 18.5% 21.2% 17.6% 23.3% 23.8% 23.9% ($ in millions) $219 $280 $325 $197 $307 $432 $513 $562 PF2017A PF2018A PF2019A 2020F 2021F 2022F 2023F 2024F

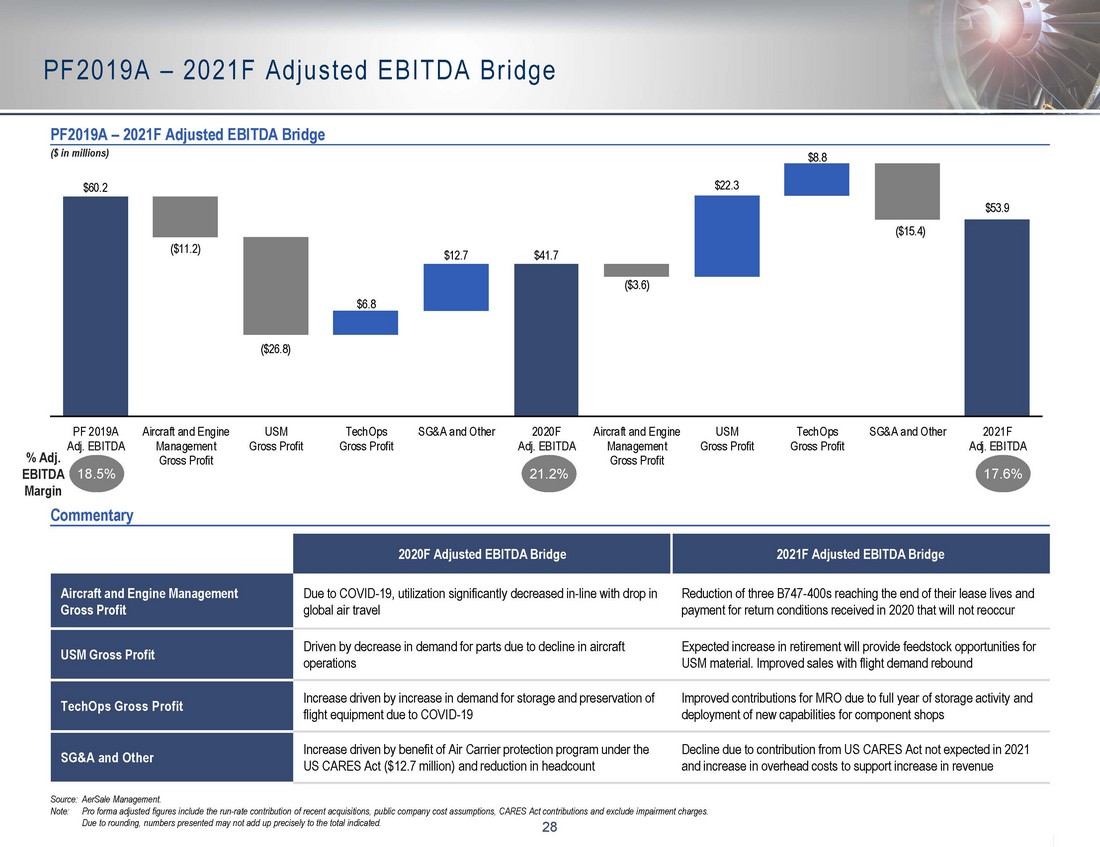

28 PF2019A – 2021F Adjusted EBITDA Bridge Source: AerSale Management. Note: Pro forma adjusted figures include the run - rate contribution of recent acquisitions, public company cost assumptions, CAR ES Act contributions and exclude impairment charges. Due to rounding, numbers presented may not add up precisely to the total indicated. PF2019A – 2021F Adjusted EBITDA Bridge Commentary 18.5% 17.6% ($ in millions) 21.2% 2020F Adjusted EBITDA Bridge 2021F Adjusted EBITDA Bridge Aircraft and Engine Management Gross Profit Due to COVID - 19, utilization significantly decreased in - line with drop in global air travel Reduction of three B747 - 400s reaching the end of their lease lives and payment for return conditions received in 2020 that will not reoccur USM Gross Profit Driven by decrease in demand for parts due to decline in aircraft operations Expected increase in retirement will provide feedstock opportunities for USM material. Improved sales with flight demand rebound TechOps Gross Profit Increase driven by increase in demand for storage and preservation of flight equipment due to COVID - 19 Improved contributions for MRO due to full year of storage activity and deployment of new capabilities for component shops SG&A and Other Increase driven by benefit of Air Carrier protection program under the US CARES Act ($12.7 million) and reduction in headcount Decline due to contribution from US CARES Act not expected in 2021 and increase in overhead costs to support increase in revenue % Adj. EBITDA Margin $60.2 $41.7 $53.9 ($11.2) ($26.8) $6.8 $12.7 ($3.6) $22.3 $8.8 ($15.4) PF 2019A Adj. EBITDA Aircraft and Engine Management Gross Profit USM Gross Profit TechOps Gross Profit SG&A and Other 2020F Adj. EBITDA Aircraft and Engine Management Gross Profit USM Gross Profit TechOps Gross Profit SG&A and Other 2021F Adj. EBITDA

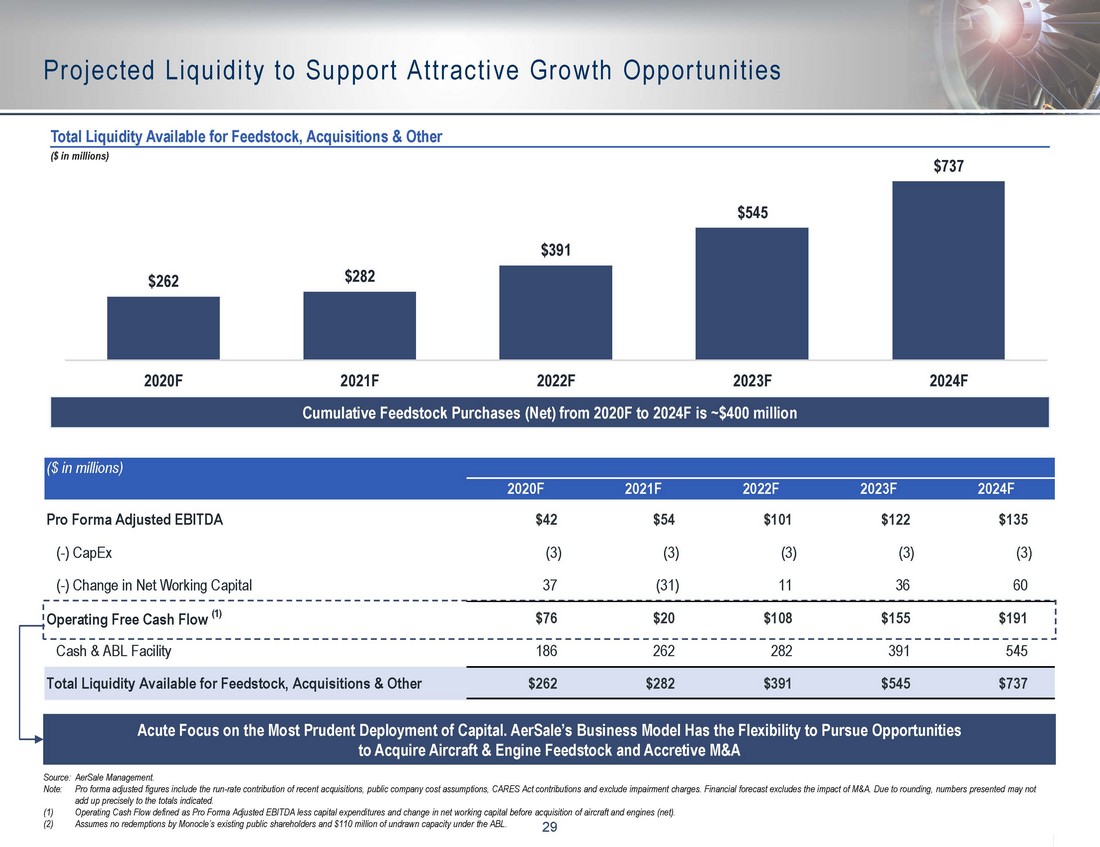

29 Projected Liquidity to Support Attractive Growth Opportunities Source: AerSale Management. Note: Pro forma adjusted figures include the run - rate contribution of recent acquisitions, public company cost assumptions, CAR ES Act contributions and exclude impairment charges. Financial forecast excludes the impact of M&A. Due to rounding, numbers pre sented may not add up precisely to the totals indicated. (1) Operating Cash Flow defined as Pro Forma Adjusted EBITDA less capital expenditures and change in net working capital before a cqu isition of aircraft and engines (net). (2) Assumes no redemptions by Monocle’s existing public shareholders and $110 million of undrawn capacity under the ABL. Total Liquidity Available for Feedstock, Acquisitions & Other ($ in millions) Acute Focus on the Most Prudent Deployment of Capital. AerSale’s Business Model Has the Flexibility to Pursue Opportunities to Acquire Aircraft & Engine Feedstock and Accretive M&A Cumulative Feedstock Purchases (Net) from 2020F to 2024F is ~$400 million (2) ($ in millions) 2020F 2021F 2022F 2023F 2024F Pro Forma Adjusted EBITDA $42 $54 $101 $122 $135 (-) CapEx (3) (3) (3) (3) (3) (-) Change in Net Working Capital 37 (31) 11 36 60 Operating Free Cash Flow (1) $76 $20 $108 $155 $191 Cash & ABL Facility 186 262 282 391 545 Total Liquidity Available for Feedstock, Acquisitions & Other $262 $282 $391 $545 $737 $262 $282 $391 $545 $737 2020F 2021F 2022F 2023F 2024F

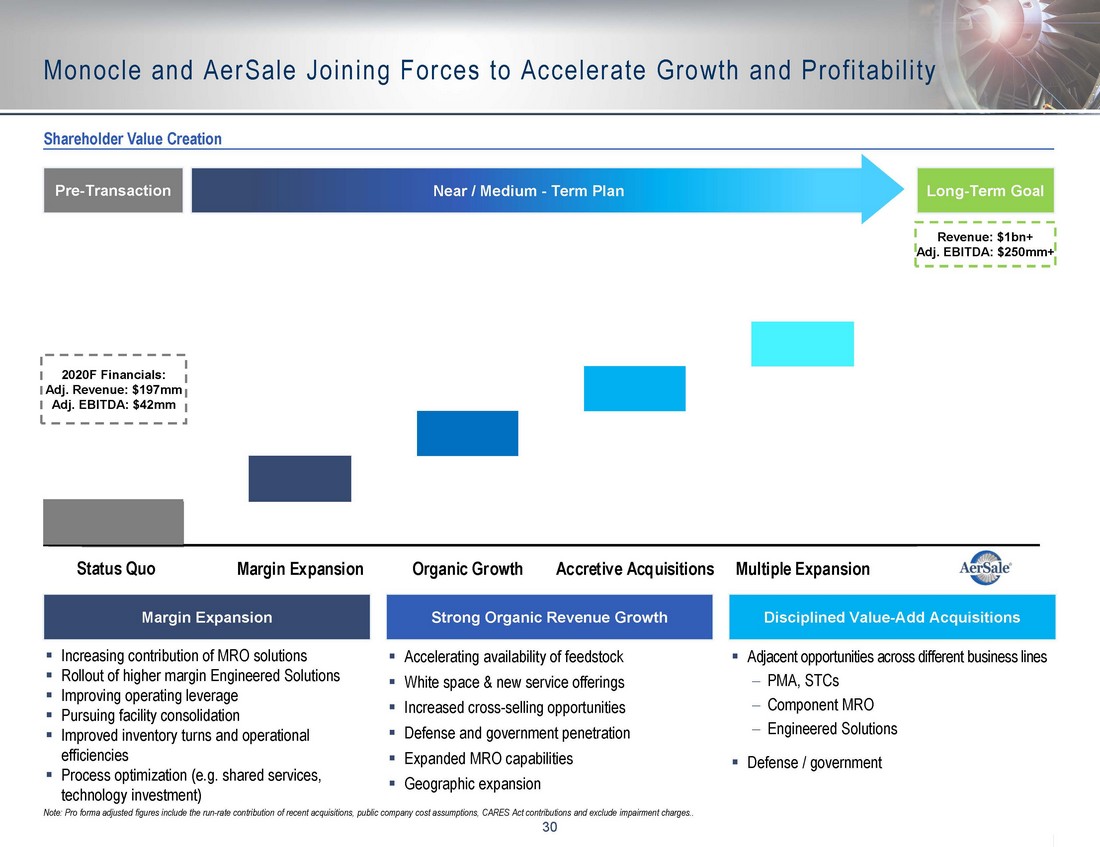

30 Current Status Margin Expansion Organic Growth Accretive Acquisitions Multiple Expansion Shareholder Value Creation Monocle and AerSale Joining Forces to Accelerate Growth and Profitability Margin Expansion Strong Organic Revenue Growth Disciplined Value - Add Acquisitions ▪ Increasing contribution of MRO solutions ▪ Rollout of higher margin Engineered Solutions ▪ Improving operating leverage ▪ Pursuing facility consolidation ▪ Improved inventory turns and operational efficiencies ▪ Process optimization (e.g. shared services, technology investment) ▪ Accelerating availability of feedstock ▪ White space & new service offerings ▪ Increased cross - selling opportunities ▪ Defense and government penetration ▪ Expanded MRO capabilities ▪ Geographic expansion ▪ Adjacent opportunities across different business lines PMA, STCs Component MRO Engineered Solutions ▪ Defense / government Pre - Transaction Near / Medium - Term Plan Long - Term Goal 2020F Financials: Adj. Revenue: $197mm Adj. EBITDA: $42mm Revenue: $1bn+ Adj. EBITDA: $250mm+ Note: Pro forma adjusted figures include the run - rate contribution of recent acquisitions, public company cost assumptions, CARE S Act contributions and exclude impairment charges.. Targets: 25% - 28% Adj. EBITDA Margin 5% - 7% Organic Growth 10% - 15% Growth from M&A Status Quo

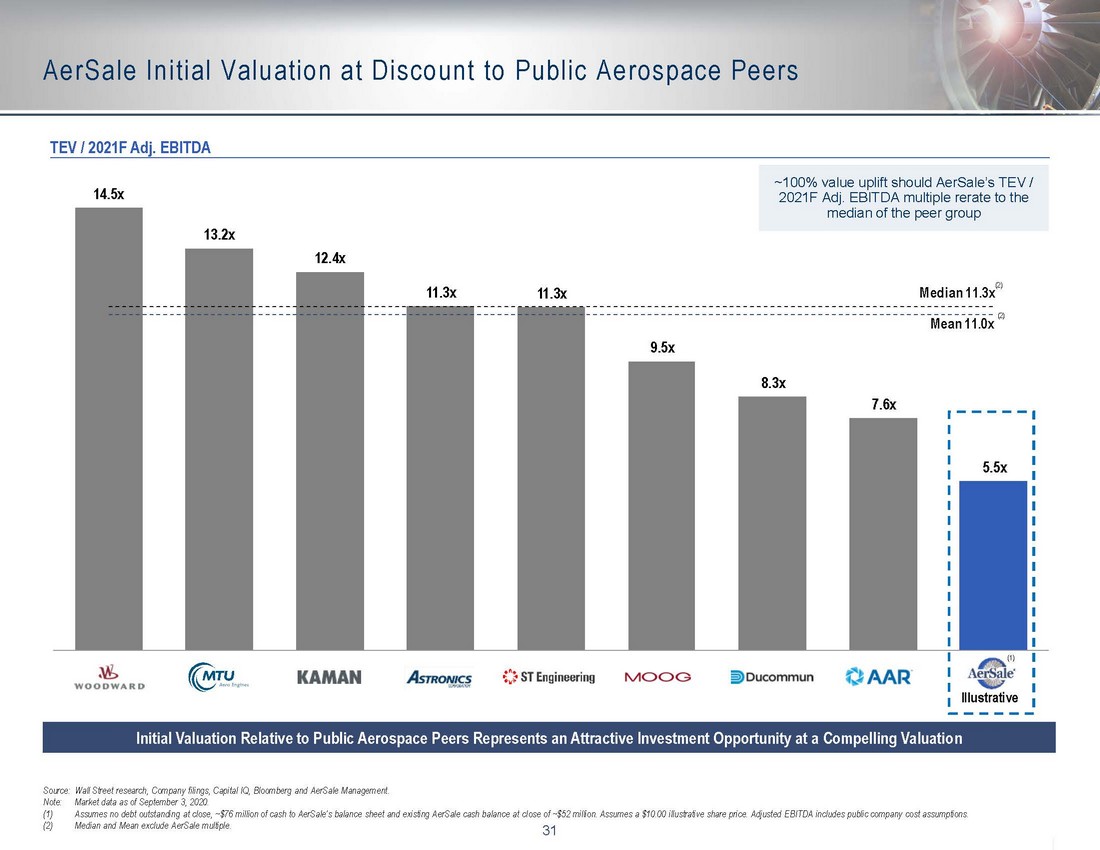

31 15.0x 13.3x 12.5x 11.7x 11.6x 9.4x 8.4x 7.6x 5.5x Median 11.6x Mean 11.2x AerSale Initial Valuation at Discount to Public Aerospace Peers 31 Source: Wall Street research, Company filings, Capital IQ, Bloomberg and AerSale Management. Note: Market data as of August 26, 2020. (1) Assumes no debt outstanding at close, ~$76 million of cash to AerSale’s balance sheet and existing AerSale cash balance at cl ose of ~$52 million. Assumes a $10.00 illustrative share price. Adjusted EBITDA includes public company cost assumptions. (2) Median and Mean exclude AerSale multiple. TEV / 2021F Adj. EBITDA ~109% value uplift should AerSale’s TEV / 2021F Adj. EBITDA multiple rerate to the median of the peer group Illustrative (2) Initial Valuation Relative to Public Aerospace Peers Represents an Attractive Investment Opportunity at a Compelling Valuatio n (1) (2)

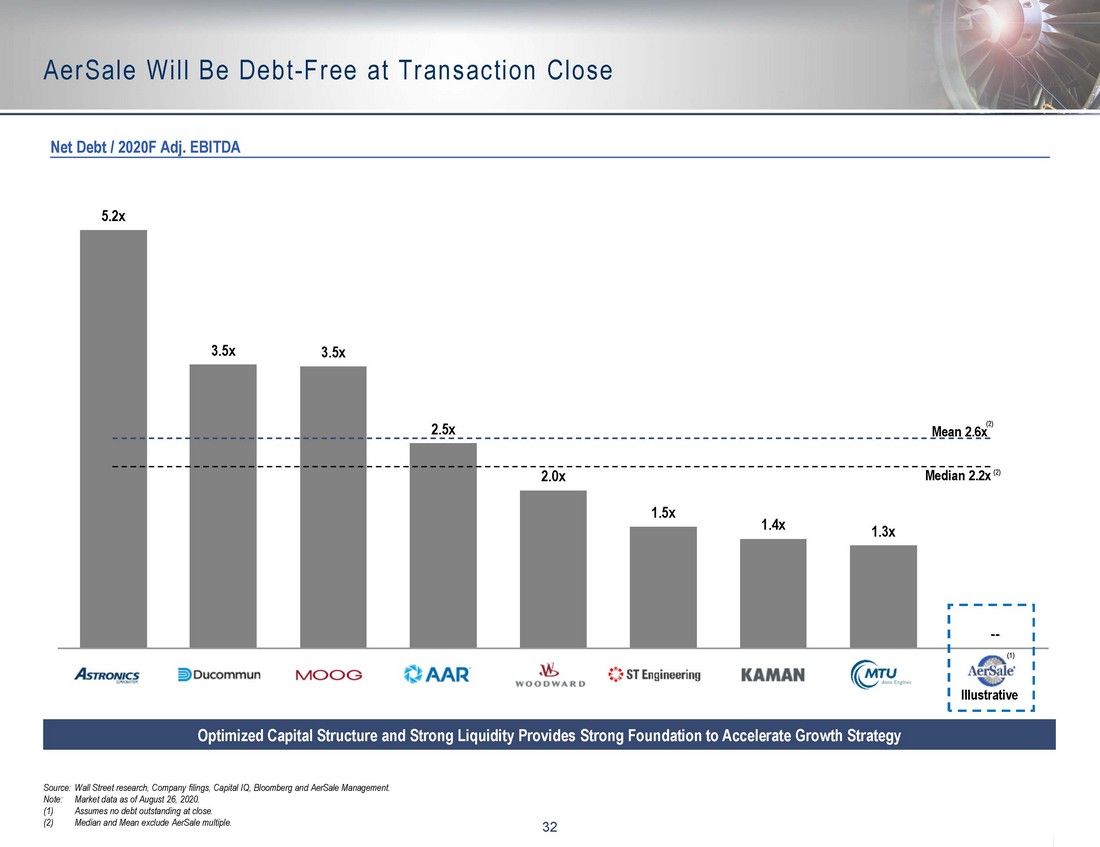

32 5.2x 3.5x 3.5x 2.5x 2.0x 1.5x 1.4x 1.3x -- Mean 2.6x Median 2.2x AerSale Will Be Debt - Free at Transaction Close 32 Source: Wall Street research, Company filings, Capital IQ, Bloomberg and AerSale Management. Note: Market data as of August 26, 2020. (1) Assumes no debt outstanding at close. (2) Median and Mean exclude AerSale multiple. Net Debt / 2020F Adj. EBITDA Illustrative (2) Optimized Capital Structure and Strong Liquidity Provides Strong Foundation to Accelerate Growth Strategy (1) (2)

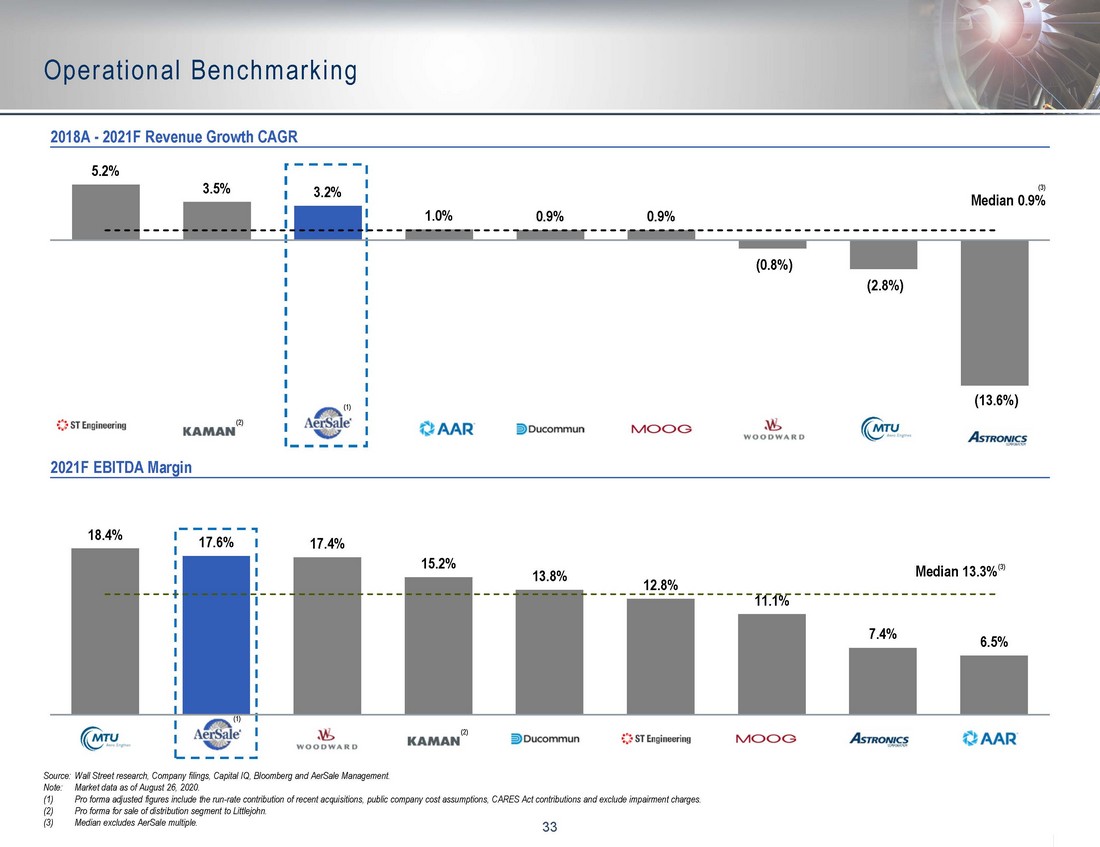

33 Operational Benchmarking 2018A - 2021F Revenue Growth CAGR 2021F EBITDA Margin (2) (3) (3) (1) (1) (2) Source: Wall Street research, Company filings, Capital IQ, Bloomberg and AerSale Management. Note: Market data as of August 26, 2020. (1) Pro forma adjusted figures include the run - rate contribution of recent acquisitions, public company cost assumptions, CARES Act contributions and exclude impairment charges. (2) Pro forma for sale of distribution segment to Littlejohn. (3) Median excludes AerSale multiple. 5.2% 3.5% 3.2% 1.0% 0.9% 0.9% (0.8%) (2.8%) (13.6%) Median 0.9% 18.4% 17.6% 17.4% 15.2% 13.8% 12.8% 11.1% 7.4% 6.5% Median 13.3%

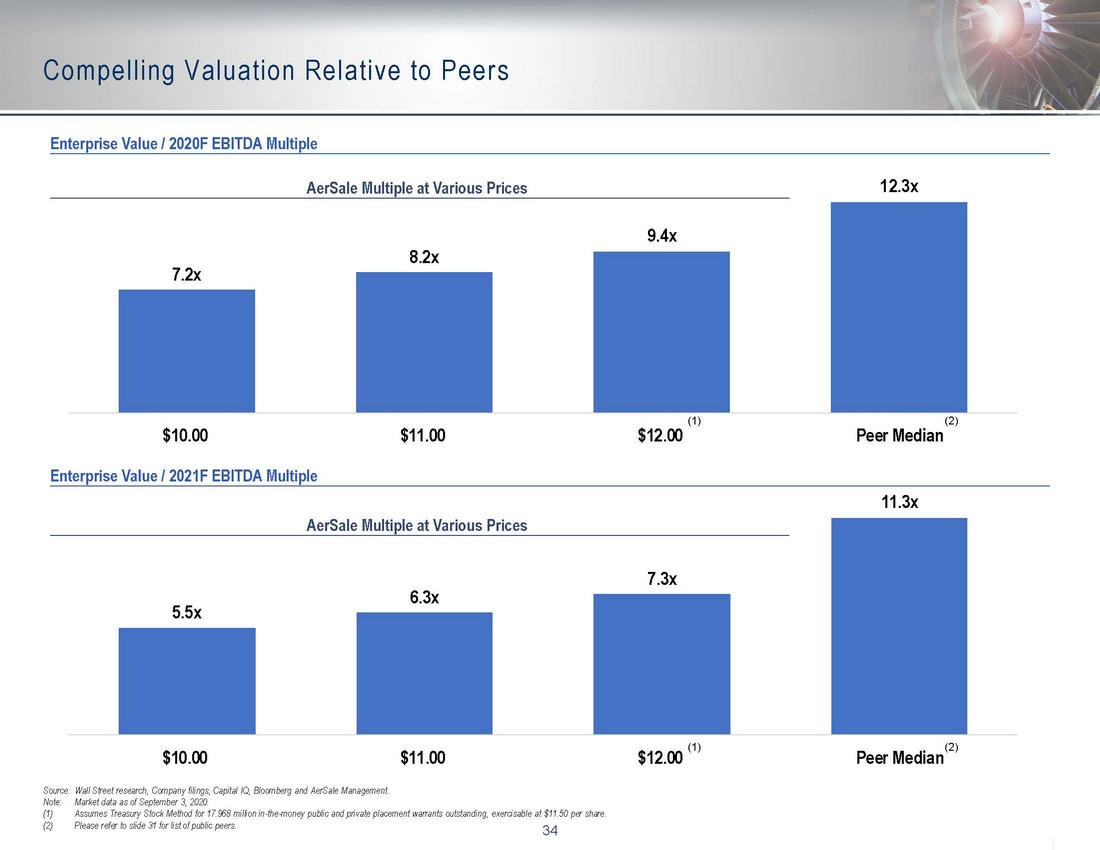

34 Compelling Valuation Relative to Peers 34 Source: Wall Street research, Company filings, Capital IQ, Bloomberg and AerSale Management. Note: Market data as of August 26, 2020. (1) Assumes Treasury Stock Method for 17.968 million in - the - money public and private placement warrants outstanding, exercisable at $11.50 per share. (2) Please refer to slide 31 for list of public peers. Enterprise Value / 2020F EBITDA Multiple Enterprise Value / 2021F EBITDA Multiple (1) (2) AerSale Multiple at Various Prices AerSale Multiple at Various Prices (1) (2) 7.2x 8.2x 9.4x 12.7x $10.00 $11.00 $12.00 Peer Median 5.5x 6.3x 7.3x 11.7x $10.00 $11.00 $12.00 Peer Median

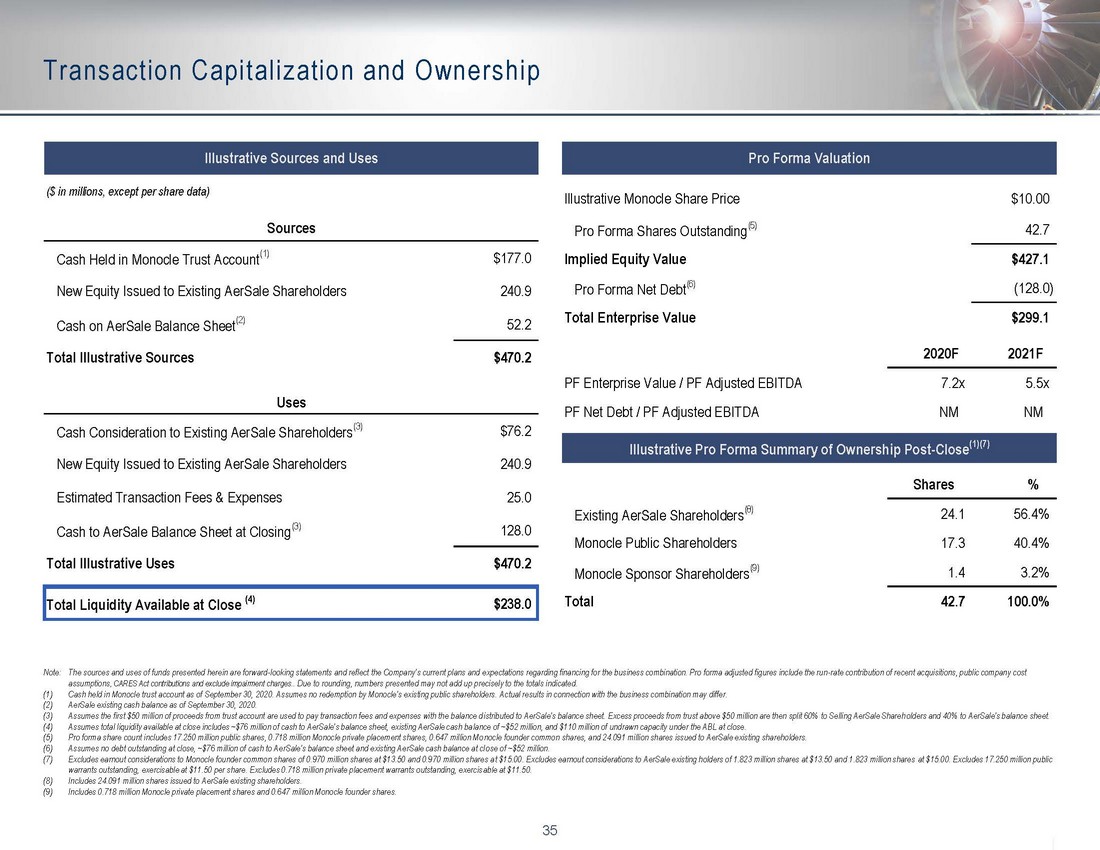

35 Transaction Capitalization and Ownership Note: The sources and uses of funds presented herein are forward - looking statements and reflect the Company’s current plans and expectations regarding financing for the business combination. Pro forma adjusted figures include the run - rate contribution of r ecent acquisitions, public company cost assumptions , CARES Act contributions and exclude impairment charges. . Due to rounding, numbers presented may not add up precisely to the totals indicated. (1) Cash held in Monocle trust account as of September 30, 2020. Assumes no redemption by Monocle’s existing public shareholders. Ac tual results in connection with the business combination may differ. (2) AerSale existing cash balance as of September 30, 2020. (3) Assumes the first $50 million of proceeds from trust account are used to pay transaction fees and expenses with the balance d ist ributed to AerSale’s balance sheet. Excess proceeds from trust above $50 million are then split 60% to Selling AerSale Shareh old ers and 40% to AerSale’s balance sheet. (4) Assumes total liquidity available at close includes ~$76 million of cash to AerSale’s balance sheet, existing AerSale cash ba lan ce of ~$52 million, and $110 million of undrawn capacity under the ABL at close. (5) Pro forma share count includes 17.250 million public shares, 0.718 million Monocle private placement shares, 0.647 million Mo noc le founder common shares, 23.877 million shares issued to AerSale existing shareholders, and 0.216 million of Monocle founder sh ares transferred to AerSale Management. (6) Assumes no debt outstanding at close, ~$76 million of cash to AerSale’s balance sheet and existing AerSale cash balance at cl ose of ~$52 million. (7) Excludes earnout considerations to Monocle founder common shares of 0.970 million shares at $13.50 and 0.970 million shares a t $ 15.00. Excludes earnout considerations to AerSale existing holders of 1.500 million shares at $13.50 and 1.500 million shares at $15.00. Excludes 0.647 million Monocle founder shares that will be transferred to AerSale Management, where 50% of the shares vest at $13.50 and at $15.00. Excludes 17 .250 million public warrants outstanding, exercisable at $11.50 per share. Excludes 0.718 million private placement warrants out standing, exercisable at $11.50. (8) Includes 23.877 million shares issued to AerSale existing shareholders and 0.216 million of Monocle founder shares transferre d t o AerSale Management. (9) Includes 0.718 million Monocle private placement shares and 0.647 million Monocle founder shares. Illustrative Sources and Uses ($ in millions, except per share data) Sources Cash Held in Monocle Trust Account (1) $177.0 New Equity Issued to Existing AerSale Shareholders 238.8 Cash on AerSale Balance Sheet (2) 52.2 Total Illustrative Sources $468.0 Uses Cash Consideration to Existing AerSale Shareholders (3) $76.2 New Equity Issued to Existing AerSale Shareholders 238.8 Estimated Transaction Fees & Expenses 25.0 Cash to AerSale Balance Sheet at Closing (3) 128.0 Total Illustrative Uses $468.0 Total Liquidity Available at Close (4) $238.0 Pro Forma Valuation Illustrative Monocle Share Price $10.00 Pro Forma Shares Outstanding (5) 42.7 Implied Equity Value $427.1 Pro Forma Net Debt (6) (128.0) Total Enterprise Value $299.1 2020F 2021F PF Enterprise Value / PF Adjusted EBITDA 7.2x 5.5x PF Net Debt / PF Adjusted EBITDA NM NM Illustrative Pro Forma Summary of Ownership Post-Close (1)(7) Shares % Existing AerSale Shareholders (8) 24.1 56.4% Monocle Public Shareholders 17.3 40.4% Monocle Sponsor Shareholders (9) 1.4 3.2% Total 42.7 100.0%

Section IV Appendix

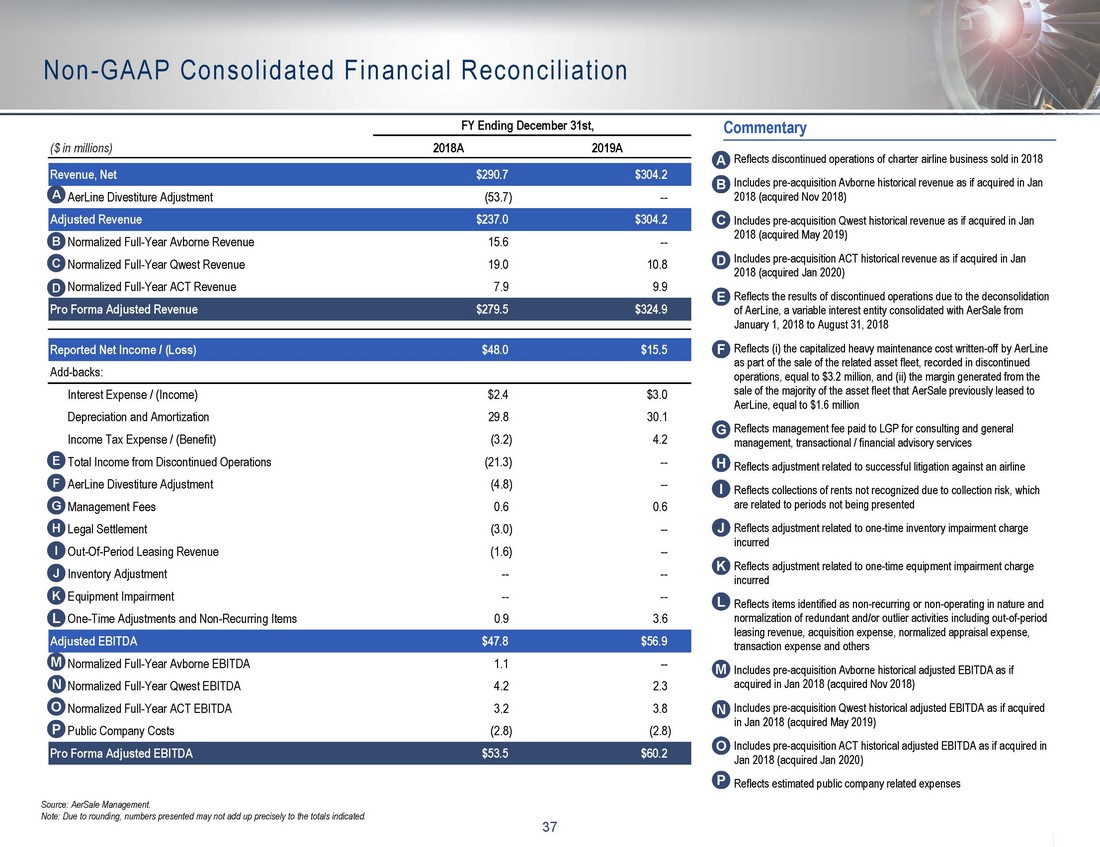

37 FY Ending December 31st, ($ in millions) 2018A 2019A Revenue, Net $290.7 $304.2 AerLine Divestiture Adjustment (53.7) -- Adjusted Revenue $237.0 $304.2 Normalized Full-Year Avborne Revenue 15.6 -- Normalized Full-Year Qwest Revenue 19.0 10.8 Normalized Full-Year ACT Revenue 7.9 9.9 Pro Forma Adjusted Revenue $279.5 $324.9 Reported Net Income / (Loss) $48.0 $15.5 Add-backs: Interest Expense / (Income) $2.4 $3.0 Depreciation and Amortization 29.8 30.1 Income Tax Expense / (Benefit) (3.2) 4.2 Total Income from Discontinued Operations (21.3) -- AerLine Divestiture Adjustment (4.8) -- Management Fees 0.6 0.6 Legal Settlement (3.0) -- Out-Of-Period Leasing Revenue (1.6) -- Inventory Adjustment -- -- Equipment Impairment -- -- One-Time Adjustments and Non-Recurring Items 0.9 3.6 Adjusted EBITDA $47.8 $56.9 Normalized Full-Year Avborne EBITDA 1.1 -- Normalized Full-Year Qwest EBITDA 4.2 2.3 Normalized Full-Year ACT EBITDA 3.2 3.8 Public Company Costs (2.8) (2.8) Pro Forma Adjusted EBITDA $53.5 $60.2 37 Non - GAAP Consolidated Financial Reconciliation A B C G I J Commentary Reflects discontinued operations of charter airline business sold in 2018 Includes pre - acquisition Avborne historical revenue as if acquired in Jan 2018 (acquired Nov 2018) Includes pre - acquisition Qwest historical revenue as if acquired in Jan 2018 (acquired May 2019) Includes pre - acquisition ACT historical revenue as if acquired in Jan 2018 (acquired Jan 2020) Reflects the results of discontinued operations due to the deconsolidation of AerLine, a variable interest entity consolidated with AerSale from January 1, 2018 to August 31, 2018 Reflects (i) the capitalized heavy maintenance cost written - off by AerLine as part of the sale of the related asset fleet, recorded in discontinued operations, equal to $3.2 million, and (ii) the margin generated from the sale of the majority of the asset fleet that AerSale previously leased to AerLine, equal to $1.6 million Reflects management fee paid to LGP for consulting and general management, transactional / financial advisory services Reflects adjustment related to successful litigation against an airline Reflects collections of rents not recognized due to collection risk, which are related to periods not being presented Reflects adjustment related to one - time inventory impairment charge incurred Reflects adjustment related to one - time equipment impairment charge incurred Reflects items identified as non - recurring or non - operating in nature and normalization of redundant and/or outlier activities including out - of - period leasing revenue, acquisition expense, normalized appraisal expense, transaction expense and others Includes pre - acquisition Avborne historical adjusted EBITDA as if acquired in Jan 2018 (acquired Nov 2018) Includes pre - acquisition Qwest historical adjusted EBITDA as if acquired in Jan 2018 (acquired May 2019) Includes pre - acquisition ACT historical adjusted EBITDA as if acquired in Jan 2018 (acquired Jan 2020) Reflects estimated public company related expenses A B C D E F G I J E D K F K H H L M N O P L M N O P Source: AerSale Management. Note: Due to rounding, numbers presented may not add up precisely to the totals indicated.

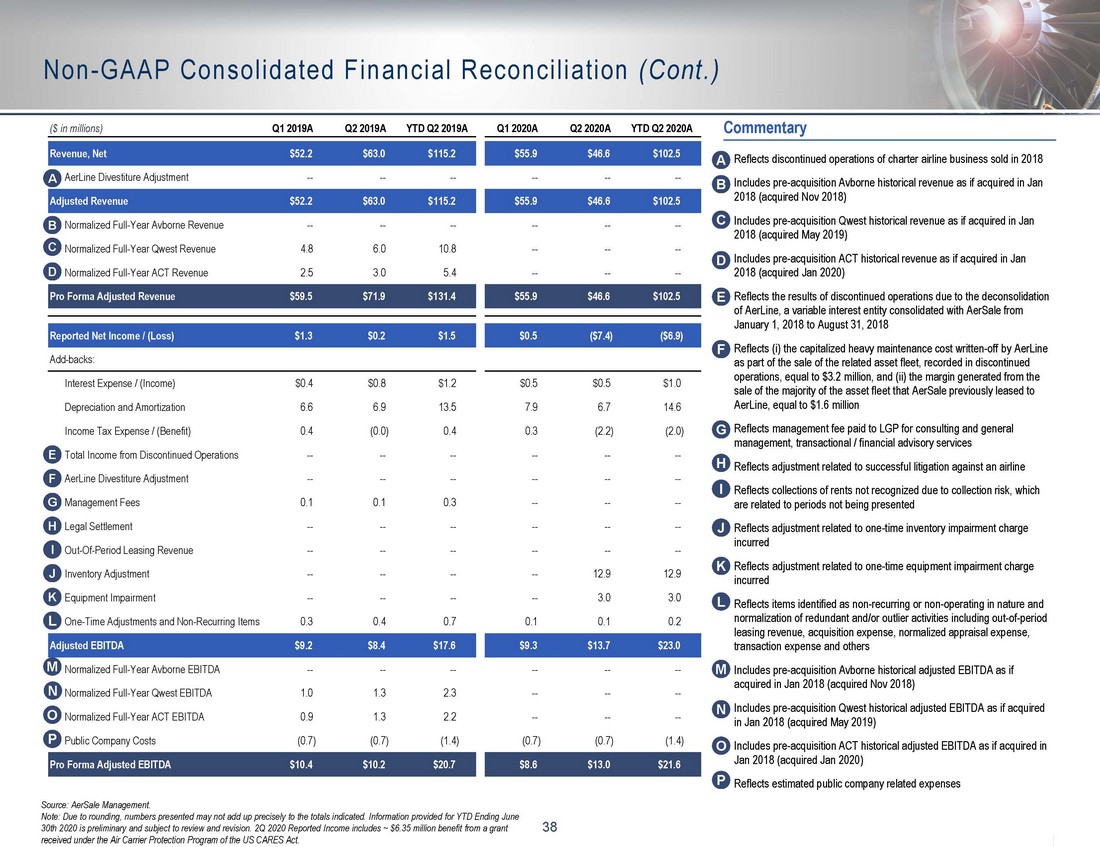

38 ($ in millions) Q1 2019A Q2 2019A YTD Q2 2019A Q1 2020A Q2 2020A YTD Q2 2020A Revenue, Net $52.2 $63.0 $115.2 $55.9 $46.6 $102.5 AerLine Divestiture Adjustment -- -- -- -- -- -- Adjusted Revenue $52.2 $63.0 $115.2 $55.9 $46.6 $102.5 Normalized Full-Year Avborne Revenue -- -- -- -- -- -- Normalized Full-Year Qwest Revenue 4.8 6.0 10.8 -- -- -- Normalized Full-Year ACT Revenue 2.5 3.0 5.4 -- -- -- Pro Forma Adjusted Revenue $59.5 $71.9 $131.4 $55.9 $46.6 $102.5 Reported Net Income / (Loss) $1.3 $0.2 $1.5 $0.5 ($7.4) ($6.9) Add-backs: Interest Expense / (Income) $0.4 $0.8 $1.2 $0.5 $0.5 $1.0 Depreciation and Amortization 6.6 6.9 13.5 7.9 6.7 14.6 Income Tax Expense / (Benefit) 0.4 (0.0) 0.4 0.3 (2.2) (2.0) Total Income from Discontinued Operations -- -- -- -- -- -- AerLine Divestiture Adjustment -- -- -- -- -- -- Management Fees 0.1 0.1 0.3 -- -- -- Legal Settlement -- -- -- -- -- -- Out-Of-Period Leasing Revenue -- -- -- -- -- -- Inventory Adjustment -- -- -- -- 12.9 12.9 Equipment Impairment -- -- -- -- 3.0 3.0 One-Time Adjustments and Non-Recurring Items 0.3 0.4 0.7 0.1 0.1 0.2 Adjusted EBITDA $9.2 $8.4 $17.6 $9.3 $13.7 $23.0 Normalized Full-Year Avborne EBITDA -- -- -- -- -- -- Normalized Full-Year Qwest EBITDA 1.0 1.3 2.3 -- -- -- Normalized Full-Year ACT EBITDA 0.9 1.3 2.2 -- -- -- Public Company Costs (0.7) (0.7) (1.4) (0.7) (0.7) (1.4) Pro Forma Adjusted EBITDA $10.4 $10.2 $20.7 $8.6 $13.0 $21.6 Non - GAAP Consolidated Financial Reconciliation (Cont.) A B C G I J E D K F H L M N O P Source: AerSale Management. Note: Due to rounding, numbers presented may not add up precisely to the totals indicated. Information provided for YTD Endin g J une 30th 2020 is preliminary and subject to review and revision. 2Q 2020 Reported Income includes ~ $6.35 million benefit from a gra nt received under the Air Carrier Protection Program of the US CARES Act. 38 Commentary A B C D E F G I J K H L M N O P Reflects discontinued operations of charter airline business sold in 2018 Includes pre - acquisition Avborne historical revenue as if acquired in Jan 2018 (acquired Nov 2018) Includes pre - acquisition Qwest historical revenue as if acquired in Jan 2018 (acquired May 2019) Includes pre - acquisition ACT historical revenue as if acquired in Jan 2018 (acquired Jan 2020) Reflects the results of discontinued operations due to the deconsolidation of AerLine, a variable interest entity consolidated with AerSale from January 1, 2018 to August 31, 2018 Reflects (i) the capitalized heavy maintenance cost written - off by AerLine as part of the sale of the related asset fleet, recorded in discontinued operations, equal to $3.2 million, and (ii) the margin generated from the sale of the majority of the asset fleet that AerSale previously leased to AerLine, equal to $1.6 million Reflects management fee paid to LGP for consulting and general management, transactional / financial advisory services Reflects adjustment related to successful litigation against an airline Reflects collections of rents not recognized due to collection risk, which are related to periods not being presented Reflects adjustment related to one - time inventory impairment charge incurred Reflects adjustment related to one - time equipment impairment charge incurred Reflects items identified as non - recurring or non - operating in nature and normalization of redundant and/or outlier activities including out - of - period leasing revenue, acquisition expense, normalized appraisal expense, transaction expense and others Includes pre - acquisition Avborne historical adjusted EBITDA as if acquired in Jan 2018 (acquired Nov 2018) Includes pre - acquisition Qwest historical adjusted EBITDA as if acquired in Jan 2018 (acquired May 2019) Includes pre - acquisition ACT historical adjusted EBITDA as if acquired in Jan 2018 (acquired Jan 2020) Reflects estimated public company related expenses

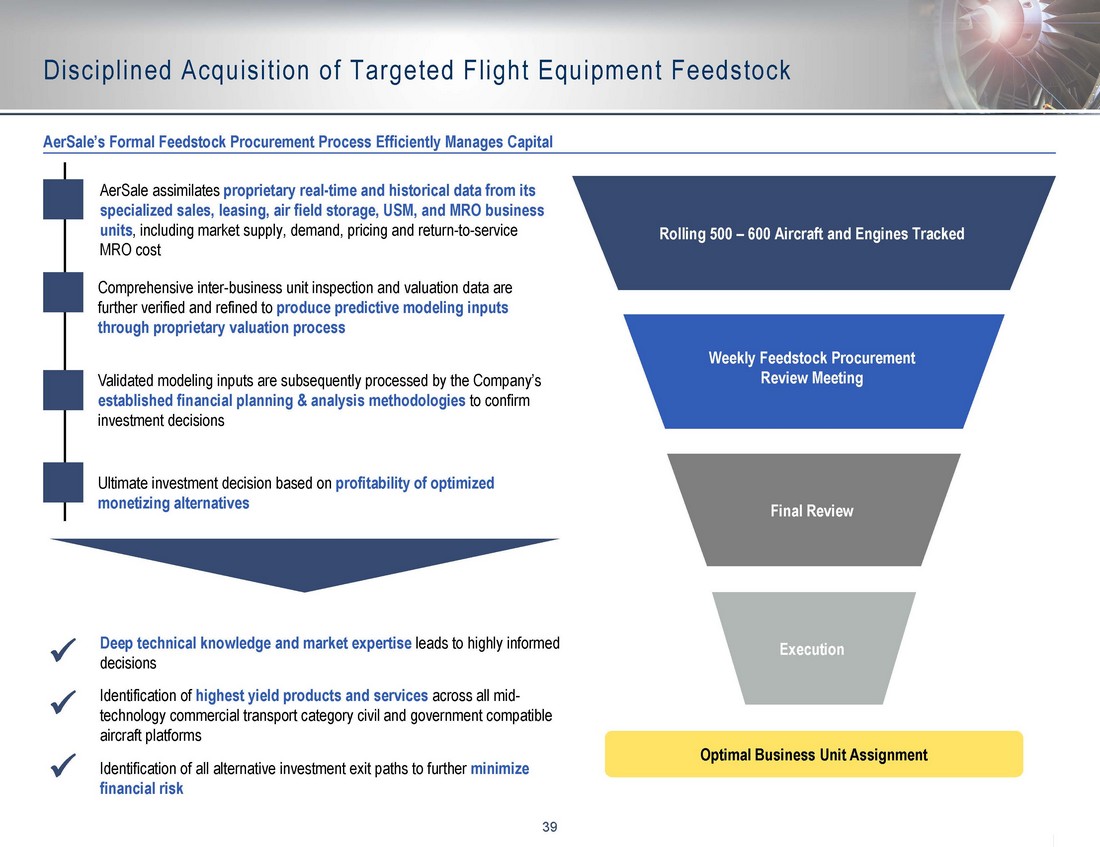

39 Disciplined Acquisition of Targeted Flight Equipment Feedstock AerSale’s Formal Feedstock Procurement Process Efficiently Manages Capital Optimal Business Unit Assignment Rolling 500 – 600 Aircraft and Engines Tracked Weekly Feedstock Procurement Review Meeting Final Review Execution AerSale assimilates proprietary real - time and historical data from its specialized sales, leasing, air field storage, USM, and MRO business units , including market supply, demand, pricing and return - to - service MRO cost Validated modeling inputs are subsequently processed by the Company’s established financial planning & analysis methodologies to confirm investment decisions Comprehensive inter - business unit inspection and valuation data are further verified and refined to produce predictive modeling inputs through proprietary valuation process Ultimate investment decision based on profitability of optimized monetizing alternatives Deep technical knowledge and market expertise leads to highly informed decisions x Identification of highest yield products and services across all mid - technology commercial transport category civil and government compatible aircraft platforms x Identification of all alternative investment exit paths to further minimize financial risk x

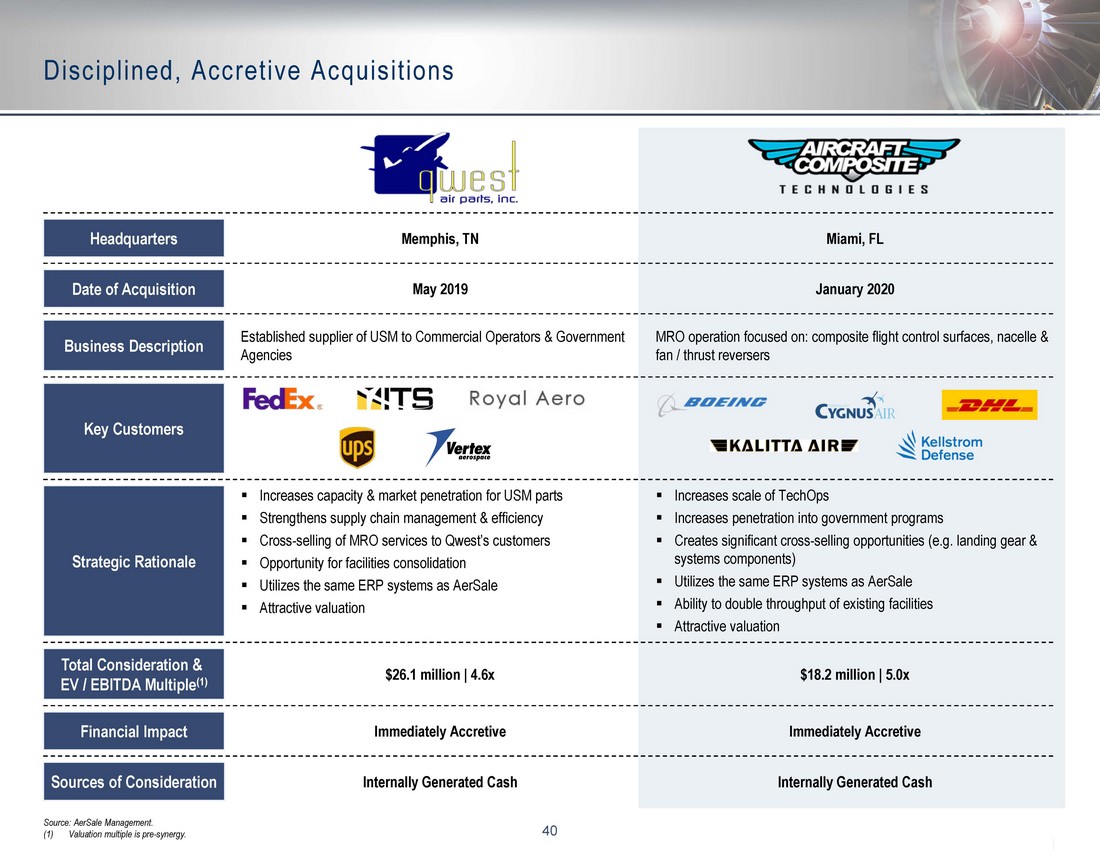

40 40 Disciplined, Accretive Acquisitions Business Description Established supplier of USM to Commercial Operators & Government Agencies MRO operation focused on: composite flight control surfaces, nacelle & fan / thrust reversers Date of Acquisition January 2020 May 2019 Headquarters Miami, FL Memphis, TN Key Customers Strategic Rationale ▪ Increases capacity & market penetration for USM parts ▪ Strengthens supply chain management & efficiency ▪ Cross - selling of MRO services to Qwest’s customers ▪ Opportunity for facilities consolidation ▪ Utilizes the same ERP systems as AerSale ▪ Attractive valuation ▪ Increases scale of TechOps ▪ Increases penetration into government programs ▪ Creates significant cross - selling opportunities (e.g. landing gear & systems components) ▪ Utilizes the same ERP systems as AerSale ▪ Ability to double throughput of existing facilities ▪ Attractive valuation Total Consideration & EV / EBITDA Multiple (1) $26.1 million | 4.6x $18.2 million | 5.0x Financial Impact Immediately Accretive Immediately Accretive Sources of Consideration Internally Generated Cash Internally Generated Cash Source: AerSale Management. (1) Valuation multiple is pre - synergy.